In this section you will find all localised and ready-to-use digital marketing materials for each of Klarna’s live markets.

Use the navigation below or on the right to jump to the market you want to activate your campaign in. Every market section contains following assets in your local language(s):

Pre-approved messaging for each of the available payment methods.

Ready-made advertising banners, based on the pre-approved messaging and including necessary legal disclosures, available to download in various desktop and mobile formats.

Ready-made email templates, available to downloadfor both launch and abandoned cart activations.

Brand kit, including Klarna badge and partner logo lockups (in local languages) for easy access in addition to the brand guidelines section.

To create a Klarna landing page please follow these instructions, which will allow you to directly integrate a dedicated page in your local language, with payment methods activated on your site and relevant FAQs.

Please utilize the pre-approved messaging options provided below, which already include essential legal disclaimers. It is crucial to also thoroughly review the advertising legal guidelines to guarantee full compliance with local promotional regulations.

Here, you'll find a variety of Klarna-approved messaging options for your marketing touchpoints or co-marketing activities in Austria. Download the ready-made asset packs provided below.

Downloadable ready-made assets

AT Generic banners.zip

2.0 MB

AT Pay Now banners.zip

456.8 KB

AT Pay Later banners.zip

450.9 KB

AT Pay in 3 banners.zip

939.6 KB

AT Brand kit (logo lock-ups) .zip

533.9 KB

AT Email templates.zip

140.1 KB

Overview of the banners and logo lockups available to download

Pay later in 30 days messaging | In bis zu 30 Tagen bezahlen

English

German

Legal disclosures

Pay flexibly in up to 30 days

Bezahle flexibel in bis zu 30 Tagen

-

Pay now or flexibly in up to 30 days

Bezahle sofort oder flexibel in bis zu 30 Tagen

-

Try now. Get 30 days to pay.

Erst anprobieren. In bis zu 30 Tagen bezahlen. (fashion only)

Erst testen. In bis zu 30 Tagen bezahlen.(other verticals)

-

Pay in 3 smaller payments messaging | 3 zinsfreie Teilzahlungen

English

German

Legal disclosures

Pay in 3 interest-free payments. With Klarna.

Bezahle in 3 zinsfreien Teilzahlungen. Mit Klarna.

-

Shop now. Pay in 3 interest-free payments with Klarna.

Jetzt shoppen. In 3 zinsfreien Teilzahlungen mit Klarna bezahlen.

-

Split your purchase into 3 interest-free payments with Klarna.

Teile deinen Kauf in 3 zinsfreie Teilzahlungen auf. Mit Klarna.

-

This section only applies to:

Here, you'll find a variety of Klarna-approved messaging options for your marketing touchpoints or co-marketing activities in Belgium. Download the ready-made asset packs provided below.

Downloadable ready-made assets

BE (French) Generic banners.zip

844.8 KB

BE (French) Pay Later banners.zip

1.3 MB

BE (French) Email templates.zip

148.4 KB

BE (Dutch) Generic banners.zip

830.5 KB

BE (Dutch) Pay Later banners.zip

947.3 KB

BE (Dutch) Email templates.zip

135.3 KB

BE Brand kit (logo lock-ups).zip

1.0 MB

Overview of the banners and logo lockups available to download

Pre-approved messaging

Generic messaging

English

Belgian French

Belgian Dutch

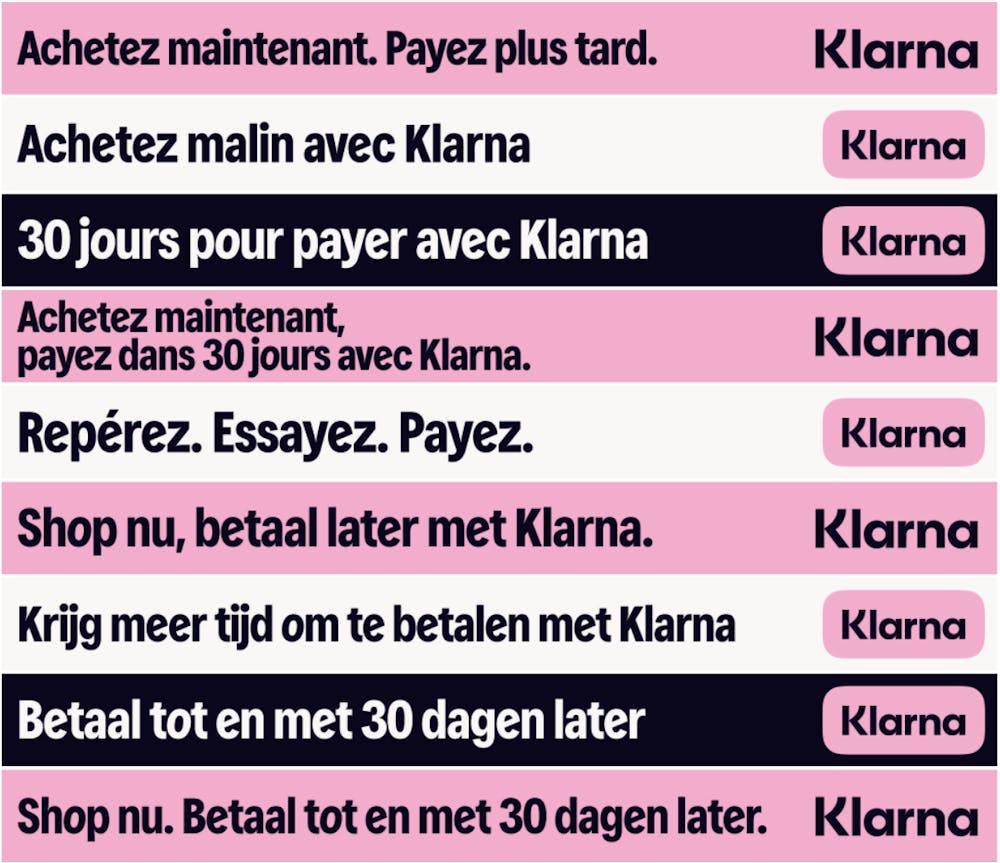

Shop now, pay later with Klarna.

Achetez maintenant, payez plus tard avec Klarna.

Shop nu, betaal later met Klarna.

Choose Klarna to pay later

Choisissez Klarna pour payer plus tard

Kies Klarna om later te betalen

Pay smarter with Klarna

Achetez malin avec Klarna

Betaal slimmer met Klarna

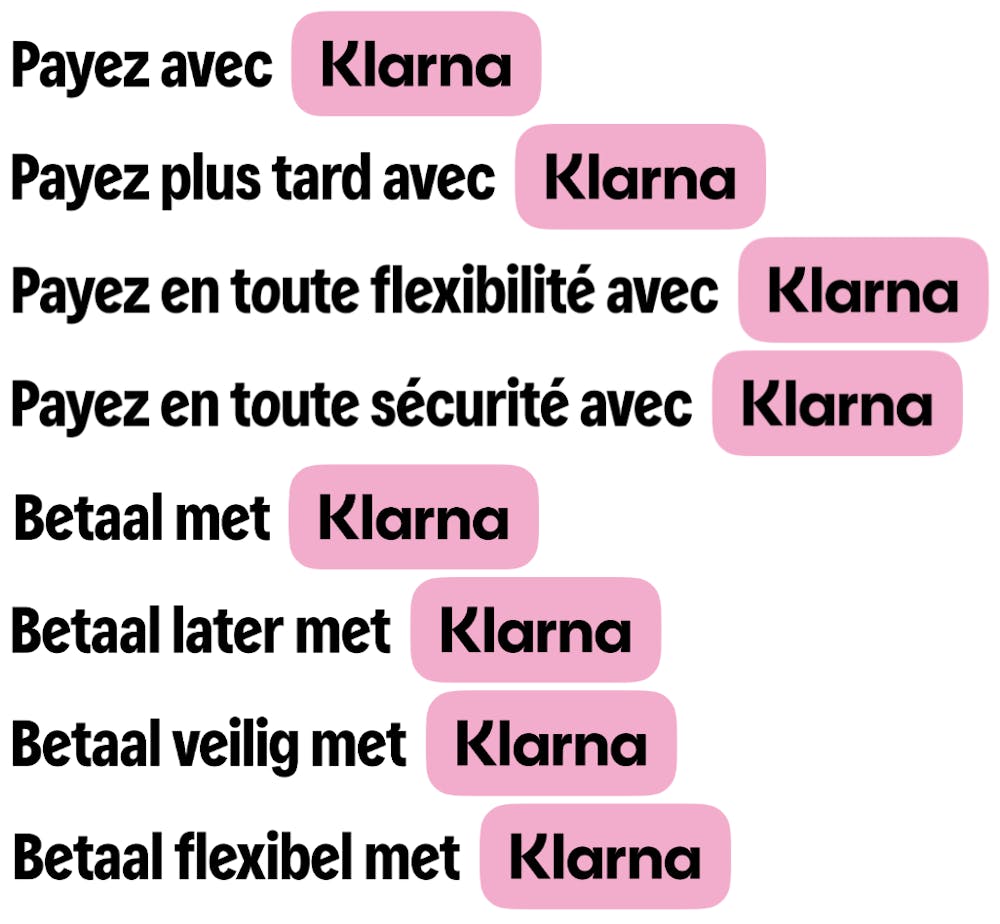

Pay flexibly with Klarna

Achetez en toute flexibilité avec Klarna

Betaal flexibel met Klarna

Pay securely with Klarna

Achetez en toute sécurité avec Klarna

Betaal veilig met Klarna

Get more time to pay with Klarna

Plus de temps pour payer avec Klarna

Krijg meer tijd om te betalen met Klarna

Pay later in 30 days messaging

English

Belgian French

Belgian Dutch

Get 30 days to pay with Klarna

30 jours pour payer avec Klarna

Betaal tot en met 30 dagen later met Klarna

Shop now. Pay in 30 days with Klarna.

Achetez maintenant, payez dans 30 jours avec Klarna.

Shop nu. Betaal tot en met 30 dagen later met Klarna.

Get it. Try it. Buy it.

Repérez. Essayez. Payez.

Ontvang het. Probeer het. Koop het.

This section only applies to:

Here, you'll find a variety of Klarna-approved messaging options for your marketing touchpoints or co-marketing activities in Czech Republic. Download the ready-made asset packs provided below.

Downloadable ready-made assets

CZ Generic banners.zip

746.2 KB

CZ Pay Now banners.zip

443.8 KB

CZ Pay Later banners.zip

424.1 KB

CZ Pay in 3 banners.zip

980.5 KB

CZ Brand kit (logo lock-ups).zip

290.5 KB

CZ Email templates.zip

150.3 KB

Overview of the banners and logo lockups available to download

Pre-approved messaging

Generic messaging

English

Czech

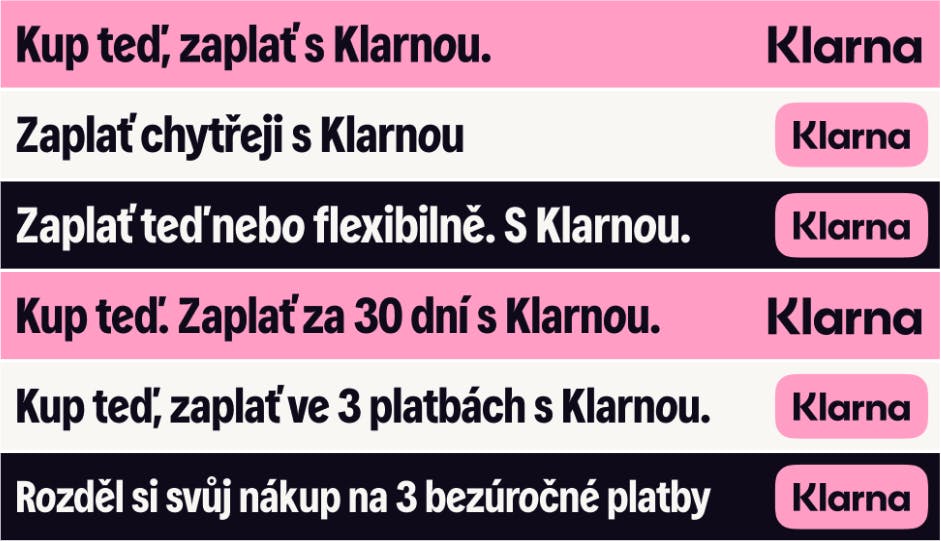

You can pay here with Klarna

Tady můžeš platit s Klarnou

Shop now, pay with Klarna.

Nakup teď, zaplať s Klarnou.

Pay smarter with Klarna

Zaplať chytřeji s Klarnou

Pay flexibly with Klarna

Zaplať flexibilně s Klarnou

Pay securely with Klarna

Zaplať bezpečně s Klarnou

Pay now messaging

English

Czech

Shop now and pay immediately

Nakup teď a zaplať okamžitě

Pay now or flexibly. With Klarna.

Zaplať teď nebo flexibilně. S Klarnou.

Pay later in 30 days messaging

English

Czech

Get 30 days to pay.

Získej 30 dní na zaplacení.

Shop now. Pay in 30 days with Klarna.

Zaplať teď. Zaplať za 30 dní s Klarnou.

Pay in 3 smaller payments messaging

English

Czech

Shop now, pay in 3 with Klarna.

Nakup teď, zaplať ve 3 platbách s Klarnou.

Split your purchases into 3 interest-free payments

Rozděl si svůj nákup na 3 bezúročné platby

Get more time to pay with Klarna

Získej více času zaplatit s Klarnou

This section only applies to:

Here, you'll find a variety of Klarna-approved messaging options for your marketing touchpoints or co-marketing activities in Denmark. Download the ready-made asset packs provided below.

Downloadable ready-made assets

DK generic banners.zip

365.0 KB

DK Pay Now banners.zip

405.2 KB

DK Pay Later banners.zip

769.9 KB

DK Pay in 3 banners.zip

791.6 KB

DK Brand kit (logo lock-ups).zip

244.1 KB

DK Email templates.zip

143.6 KB

Overview of the banners and logo lockups available to download

Pre-approved messaging

Generic messaging

English

Danish

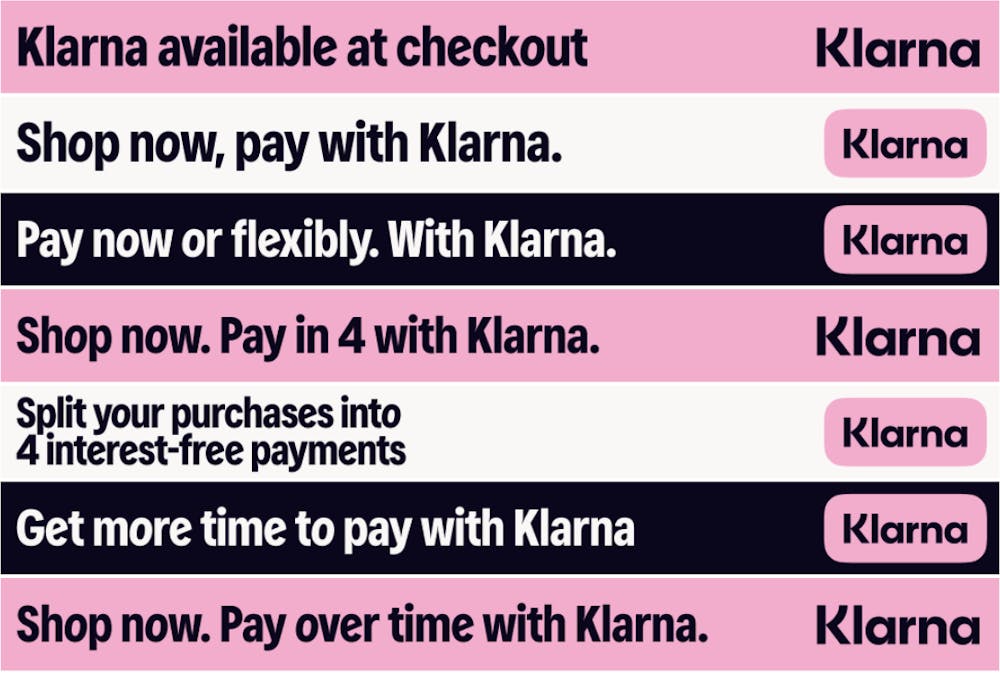

Klarna available at checkout

Klarna tilgængelig ved kassen

Shop now. Pay with Klarna.

Køb nu. Betal med Klarna.

Pay smarter with Klarna

Betal smartere med Klarna

Pay now messaging

English

Danish

Shop now and pay immediately.

Køb nu og betal med det samme.

Pay now or flexibly. With Klarna.

Betal nu eller senere. Med Klarna.

Pay later in 30 days messaging

English

Danish

Get it. Try it. Buy it.

Få det. Prøv det. Køb det.

Get 30 days to pay

Betal om 30 dage.

Shop now. Pay in 30 days with Klarna.

Køb nu. Betal om 30 dage med Klarna.

Pay in 3 smaller payments messaging

English

Danish

Shop now. Pay in 3 with Klarna.

Køb nu. Betal i 3 dele med Klarna.

Split your purchases into 3 interest-free payments.

Opdel dine køb i 3 rentefrie betalinger.

Get more time to pay with Klarna

Få mere tid til at betale med Klarna

Shop now. Pay over time with Klarna.

Køb nu. Betal senere med Klarna.

This section only applies to:

Here, you'll find a variety of Klarna-approved messaging options for your marketing touchpoints or co-marketing activities in Finland. Download the ready-made asset packs provided below.

Downloadable ready-made assets

FI Generic banners.zip

747.9 KB

FI Pay Now banners.zip

417.0 KB

FI Pay Later banners.zip

496.5 KB

FI Pay in 3 banners.zip

917.5 KB

FI Brand kit (logo lock-ups).zip

118.7 KB

FI Email templates.zip

132.8 KB

Overview of the banners and logo lockups available to download

Pre-approved messaging

Generic messaging

English

Finnish

Klarna available at checkout

Klarna käytettävissä kassalla

Shop now. Pay with Klarna.

Osta nyt. Maksa Klarnalla.

Pay securely with Klarna

Maksa turvallisesti Klarnalla

Pay now messaging

English

Finnish

Shop now. Pay immediately.

Osta nyt. Maksa heti.

Pay now or flexibly with Klarna.

Maksa heti tai myöhemmin Klarnalla.

Pay later in 30 days messaging

English

Finnish

Get it. Try it. Buy it.

Tilaa. Kokeile. Osta.

Get 30 days to pay

Saat 30 päivää maksuaikaa.

Shop now. Pay in 30 days with Klarna.

Osta nyt. Maksa 30 päivän kuluessa Klarnalla.

Pay in 3 smaller payments messaging

English

Finnish

Shop now. Pay in 3 with Klarna.

Osta nyt. Maksa 3 erässä Klarnalla.

Split your purchases into 3 interest-free payments.

Pilko ostoksesi 3 kuluttomaan ja korottomaan maksuerään.

Shop now. Pay over time with Klarna.

Osta nyt. Maksa ajan kanssa Klarnalla.

This section only applies to:

Here, you'll find a variety of Klarna-approved messaging options for your marketing touchpoints or co-marketing activities in France. Download the ready-made asset packs provided below.

Downloadable ready-made assets

FR Generic banners.zip

841.6 KB

FR Pay Later banners.zip

919.5 KB

FR Pay in 3 banners.zip

846.5 KB

FR Brand kit (logo lock-ups).zip

407.0 KB

FR Email templates.zip

143.3 KB

Overview of the banners and logo lockups available to download

Pre-approved messaging

Generic messaging — triggers disclosure for TV/OOH*

English

French

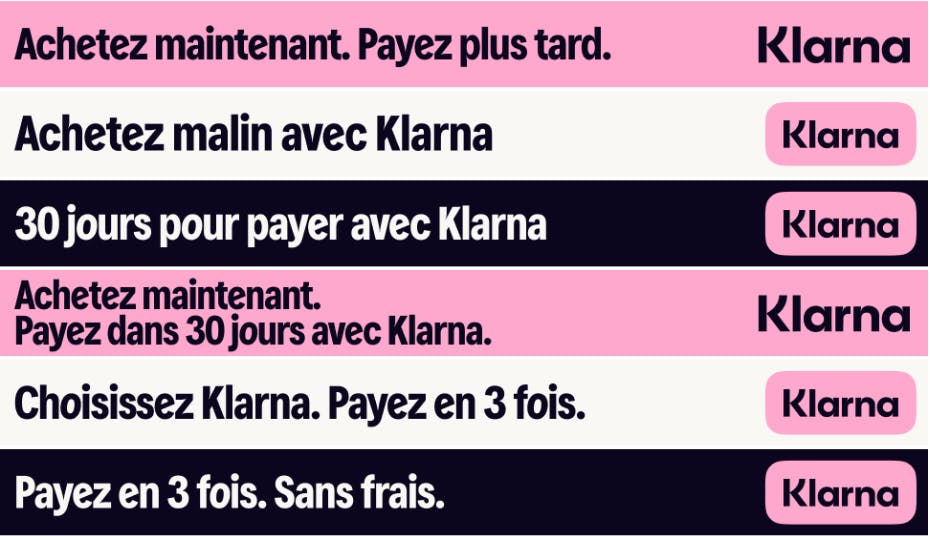

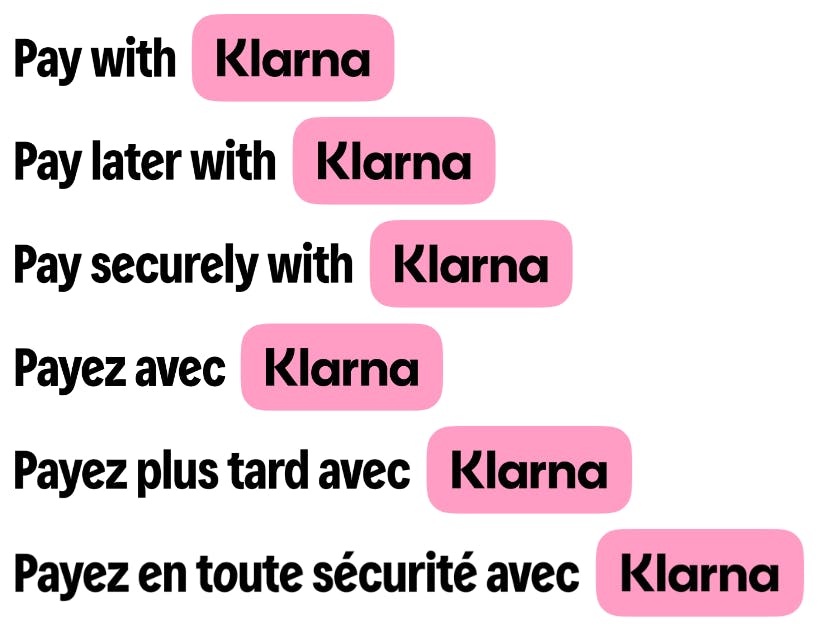

Shop now. Pay later with Klarna.

Achetez maintenant. Payez plus tard avec Klarna.

Choose Klarna to spread the cost

Choisissez Klarna pour échelonner vos paiements

Pay smarter with Klarna

Achetez malin avec Klarna

Pay flexibly with Klarna

Achetez en toute flexibilité avec Klarna

Pay securely with Klarna

Achetez en toute sécurité avec Klarna

Get more time to pay with Klarna

Plus de temps pour payer avec Klarna

Pay in 3 smaller payments messaging — triggers disclosure for TV/OOH*

English

French

Choose Klarna. Pay in 3 installments.

Choisissez Klarna. Payez en 3 fois.

Shop now. Pay in 3 interest-free installments with Klarna.

Achetez maintenant. Payez en 3 fois sans frais avec Klarna.

Pay in 3 instalments. Interest-free.

Payez en 3 fois. Sans frais.

Pay later in 30 days messaging — triggers disclosure for TV/OOH*

English

French

Get 30 days to pay with Klarna.

30 jours pour payer avec Klarna.

Get 30 days to pay

Payez 30 jours après.

Shop now. Pay in 30 days with Klarna.

Achetez maintenant. Payez dans 30 jours avec Klarna.

Get it. Try it. Buy it.

Repérez. Essayez. Payez.

*Disclosure for TV/OOH only:

Pay in 3 mention: Payez en 3 fois sous 60 jours max sans frais si échéances réglées à temps. Réservé aux personnes majeures résidant en France avec carte de débit/crédit pour des achats de 35€ à 1500€. Conditions d’éligibilité et frais de retard : klarna.com/fr/legal Klarna Bank AB, 33 rue la Fayette, 75009, Paris, France.

Pay in 30 mention: Payez dans 30 jours max sans frais si échéances réglées à temps. Réservé aux personnes majeures résidant en France avec carte de débit/crédit pour des achats de 35€ à 1500€. Conditions d’éligibilité et frais de retard : klarna.com/fr/legal Klarna Bank AB, 33 rue la Fayette, 75009, Paris, France.

This section only applies to:

Here, you'll find a variety of Klarna-approved messaging options for your marketing touchpoints or co-marketing activities in Germany. Download the ready-made asset packs provided below.

Downloadable ready-made assets

DE Generic banners.zip

2.0 MB

DE Pay Now banners.zip

457.2 KB

DE Pay Later banners.zip

451.3 KB

DE Pay in 3 banners.zip

940.4 KB

DE Financing banners.zip

501.1 KB

DE Brand kit (logo lock-ups) .zip

533.7 KB

DE Email templates.zip

137.3 KB

Overview of the banners and logo lockups available to download

Pre-approved messaging

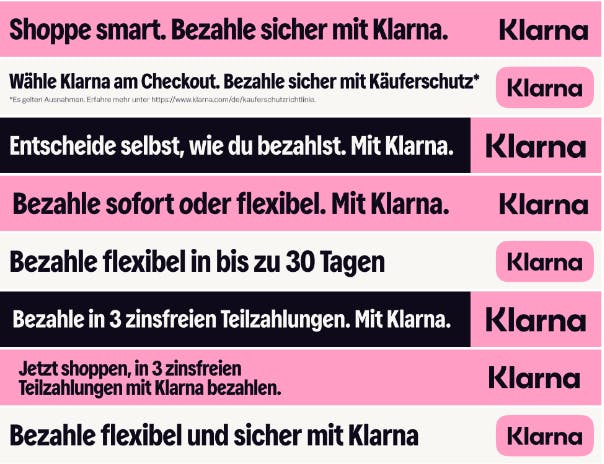

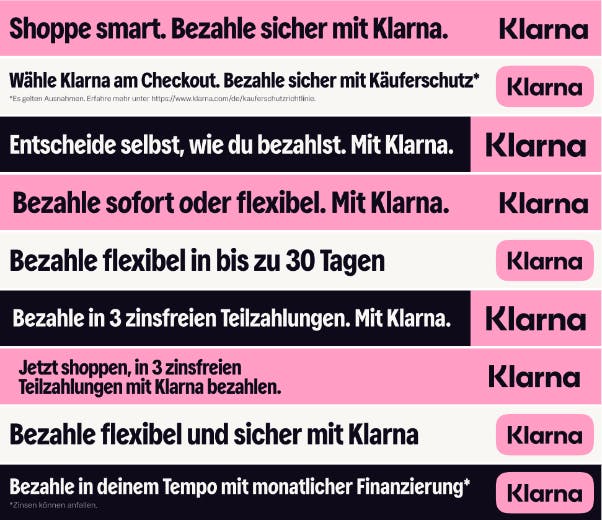

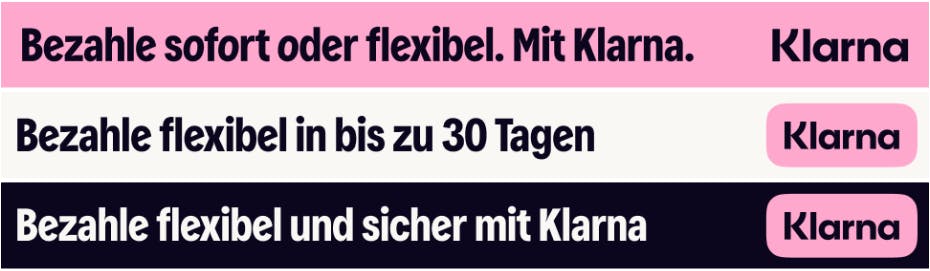

Generic messaging | Generisches Messaging

English

German

Legal disclosures

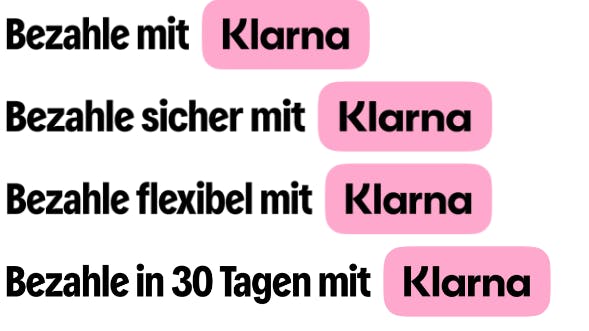

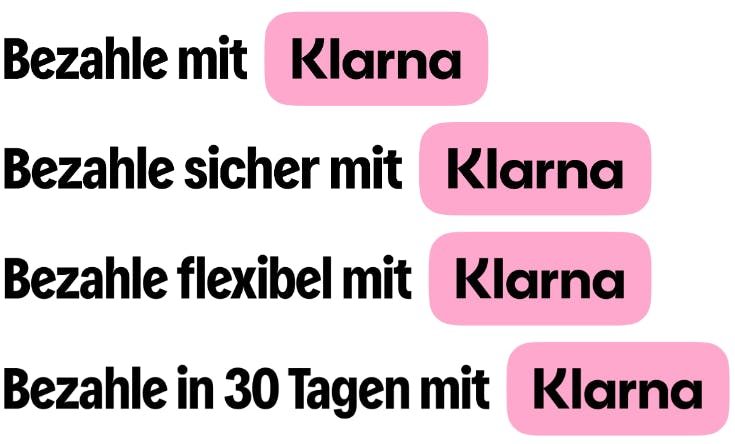

Shop now. Pay securely with Klarna.

Shoppe jetzt. Bezahle sicher mit Klarna.

-

Pay flexibly and securely with Klarna

Bezahle flexibel und sicher mit Klarna

-

You decide how you want to pay. With Klarna.

Entscheide selbst, wie du bezahlst. Mit Klarna.

-

Choose Klarna at checkout. Pay securely with buyer protection.*

*Exclusions apply. Learn more at https://www.klarna.com/de/kauferschutzrichtlinie/.

Please do not use this messaging if your brand is operating in the travel, event tickets or gift cards category.

Wähle Klarna am Checkout. Bezahle sicher mit Käuferschutz.*

*Es gelten Ausnahmen. Erfahre mehr unter https://www.klarna.com/de/kauferschutzrichtlinie/.

Pay now messaging | Sofort bezahlen

English

German

Legal disclosures

Shop now and pay immediately

Jetzt shoppen und sofort bezahlen

-

Pay now or flexibly. With Klarna.

Bezahle sofort oder flexibel. Mit Klarna.

-

Pay later in 30 days messaging | In bis zu 30 Tagen bezahlen

English

German

Legal disclosures

Shop now and pay in up to 30 days

Jetzt shoppen und in bis zu 30 Tagen bezahlen

-

Pay now or flexibly in up to 30 days

Bezahle sofort oder flexibel in bis zu 30 Tagen

-

Try now. Get 30 days to pay.

Erst anprobieren. In bis zu 30 Tagen bezahlen. (fashion only)

Erst testen. In bis zu 30 Tagen bezahlen. (other verticals)

-

Pay in 3 smaller payments messaging | 3 zinsfreie Teilzahlungen

English

German

Legal disclosures

Pay in 3 interest-free payments. With Klarna.

Bezahle in 3 zinsfreien Teilzahlungen. Mit Klarna.

-

Shop now. Pay in 3 interest-free payments with Klarna.

Jetzt shoppen. In 3 zinsfreien Teilzahlungen mit Klarna bezahlen.

-

Split your purchase into 3 interest-free payments. With Klarna.

Teile deinen Kauf in 3 zinsfreie Teilzahlungen auf. Mit Klarna.

-

This section only applies to:

Here, you'll find a variety of Klarna-approved messaging options for your marketing touchpoints or co-marketing activities in Greece. Download the ready-made asset packs provided below.

Downloadable ready-made assets

GR Generic banners.zip

920.4 KB

GR Pay Now banners.zip

448.1 KB

GR Pay Later banners.zip

985.4 KB

GR Pay in 3 banners.zip

1.6 MB

GR Brand kit (logo lockups).zip

661.5 KB

GR Email templates.zip

212.0 KB

Overview of the banners and logo lockups available to download

Pre-approved messaging

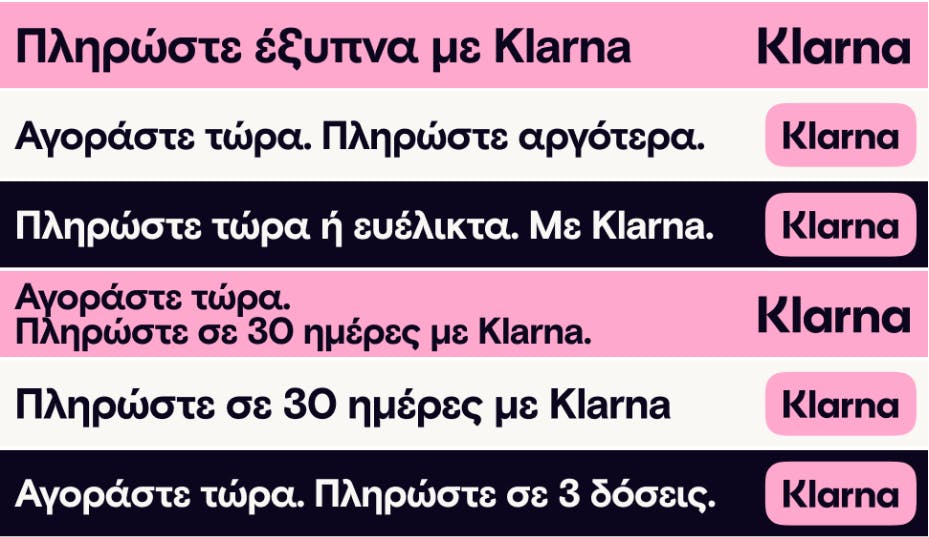

Generic messaging

English

Greek

Klarna available at checkout

Klarna διαθέσιμη στο ταμείο

Shop now. Pay with Klarna.

Αγοράστε τώρα. Πληρώστε με Klarna.

Pay smarter with Klarna

Πληρώστε έξυπνα με Klarna

Shop now. Pay over time with Klarna.

Αγοράστε τώρα. Πληρώστε αργότερα με Klarna.

Get it now. Pay it later.

Αγοράστε τώρα. Πληρώστε αργότερα.

Pay now messaging

English

Greek

Shop now and pay immediately

Αγοράστε τώρα και πληρώστε αμέσως

Pay now or flexibly. With Klarna.

Πληρώστε τώρα ή ευέλικτα. Με Klarna.

Pay later in 30 days messaging

English

Greek

Receive it before you buy. Get 30 days to pay.

Παραλάβετε πριν αγοράσετε. Πληρώστε σε 30 ημέρες.

Shop now. Pay in 30 days with Klarna.

Αγοράστε τώρα. Πληρώστε σε 30 ημέρες με Klarna.

Get 30 days to pay with Klarna

Πληρώστε σε 30 ημέρες με Klarna

Pay in 30 days. Try the new payment method by Klarna with no interest or fees.

Πληρώστε σε 30 ημέρες. Δοκιμάστε το νέο τρόπο πληρωμής από Klarna χωρίς έξοδα ή τόκους.

Pay in 3 smaller payments messaging

English

Greek

Shop now. Pay in 3 with Klarna.

Αγοράστε τώρα. Πληρώστε σε 3 δόσεις με Klarna.

Split your purchases into 3 interest-free payments.

Μοιράστε τις πληρωμές σας σε 3 άτοκες δόσεις.

Get more time to pay with Klarna

Κερδίστε περισσότερο χρόνο να πληρώσετε με Klarna

3 interest-free installments, without credit card.

3 άτοκες δόσεις, χωρίς πιστωτική κάρτα.

Pay in 3 interest-free installments, even with your debit card.

3 άτοκες δόσεις. Ακόμη και με τη χρεωστική σας κάρτα.

This section only applies to:

Here, you'll find a variety of Klarna-approved messaging options for your marketing touchpoints or co-marketing activities in Hungary. Download the ready-made asset packs provided below.

Downloadable ready-made assets

HU Generic banners.zip

827.3 KB

HU Pay Now banners.zip

512.1 KB

HU Pay Later banners.zip

504.3 KB

HU Pay in 3 banners.zip

982.1 KB

HU Brand kit (logo lock-ups).zip

574.5 KB

HU Email templates.zip

134.1 KB

Overview of the banners and logo lockups available to download

Pre-approved messaging

Generic messaging

English

Hungarian

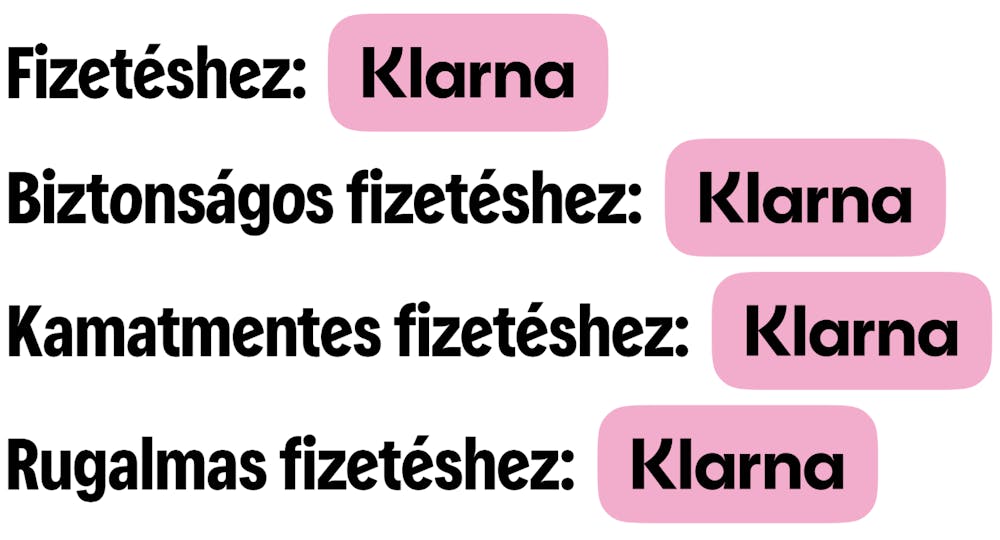

Klarna is available

A Klarna elérhető

Klarna payment is available

A Klarnás fizetés elérhető

Shop now. Pay with Klarna.

Vásárolj most. Fizess Klarnával.

Pay smarter with Klarna

Fizess okosan a Klarnával

Pay flexibly with Klarna

Fizess rugalmasan a Klarnával

Pay securely with Klarna

Fizess biztonságosan a Klarnával

Pay now messaging

English

Hungarian

Shop now, pay immediately.

Vásárolj most, fizess azonnal.

Pay now or flexibly later. With Klarna.

Fizess most vagy rugalmasan később. A Klarnával.

Pay later in 30 days messaging

English

Hungarian

Get it. Try it. Pay it.

Vedd át. Próbáld ki. Fizesd ki.

Shop now. Pay in 30 days with Klarna.

Vásárolj most. Fizess 30 napon belül a Klarnával.

Pay in 3 smaller payments messaging

English

Hungarian

Shop now, pay in 3 with Klarna.

Vásárolj most, fizess 3 részletben a Klarnával.

Split your purchases into 3 interest-free installments

Oszd fel a vásárlásod 3 kamatmentes részletre

Shop now. Pay in installments with Klarna.

Vásárolj most. Fizess részletekben a Klarnával.

This section only applies to:

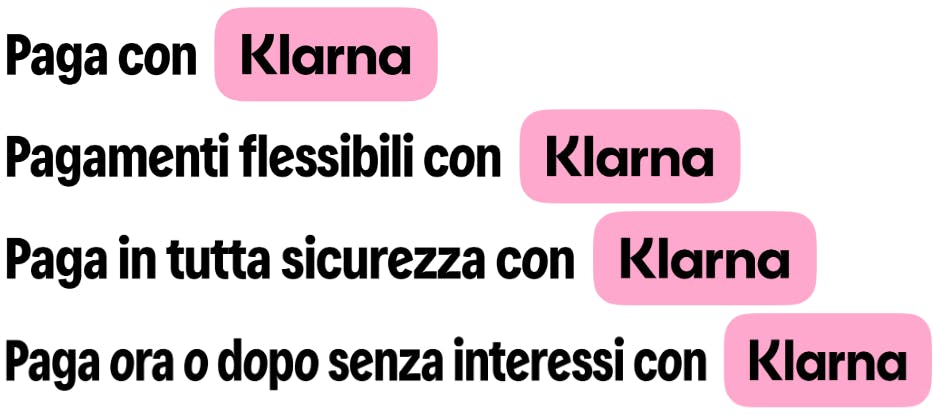

Here, you'll find a variety of Klarna-approved messaging options for your marketing touchpoints or co-marketing activities in Italy. Download the ready-made asset packs provided below.

Downloadable ready-made assets

IT Generic banners.zip

943.8 KB

IT Pay Now banners.zip

412.8 KB

IT Pay Later banners.zip

486.0 KB

IT Pay in 3 banners.zip

512.3 KB

IT Brand kit (logo lockups) .zip

601.1 KB

IT Email templates.zip

140.4 KB

Overview of the banners and logo lockups available to download

Pre-approved messaging

Generic messaging ― triggers disclosure for TV/OOH*

English

Italian

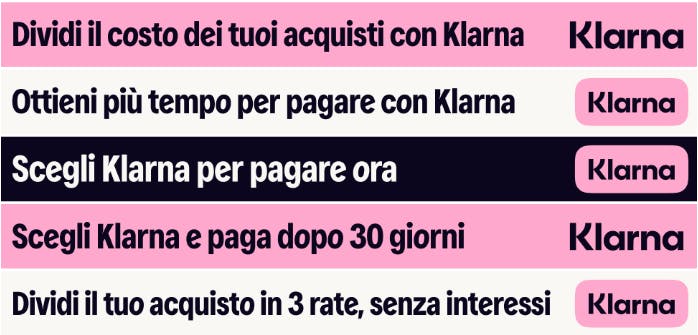

Spread the cost of your purchases with Klarna

Dividi il costo dei tuoi acquisti con Klarna

Get more time to pay with Klarna

Ottieni più tempo per pagare con Klarna

Choose Klarna to spread the cost

Scegli Klarna per dividere il costo

Pay your way with Klarna

Paga a modo tuo con Klarna

Pay in 3 messaging ― triggers disclosure for TV/OOH*

English

Italian

Choose Klarna and pay in 3 installments with no interest

Scegli Klarna e paga in 3 rate, senza interessi

Split your purchase into 3 payments with no interest

Dividi il tuo acquisto in 3 rate, senza interessi

Pay later in 30 days messaging ― triggers disclosure for TV/OOH*

English

Italian

Choose Klarna and pay in 30 days

Scegli Klarna e paga dopo 30 giorni

Get 30 days to pay with Klarna

Con Klarna, hai 30 giorni per pagare

Pay after delivery

Paga dopo la consegna

Pay now messaging

English

Italian

Pay now with Klarna

Paga ora con Klarna

Choose Klarna to pay now

Scegli Klarna per pagare ora

Pay securely, choose Klarna.

Paga in tutta sicurezza, scegli Klarna.

*Disclosure for TV only:

Messaggio pubblicitario con finalità promozionale. “Paga in 3 rate senza interessi” e "Paga dopo 30 giorni senza interessi" con Klarna sono disponibili solo per i residenti in Italia. Età minima 18 anni. La concessione della dilazione di pagamento è subordinata alla sussistenza dei necessari requisiti di idoneità. Per le condizioni relative ai prodotti pubblicizzati e per quanto non espressamente indicato si rinvia ai termini dei servizi di Klarna disponibili su www.klarna.com/it

This section only applies to:

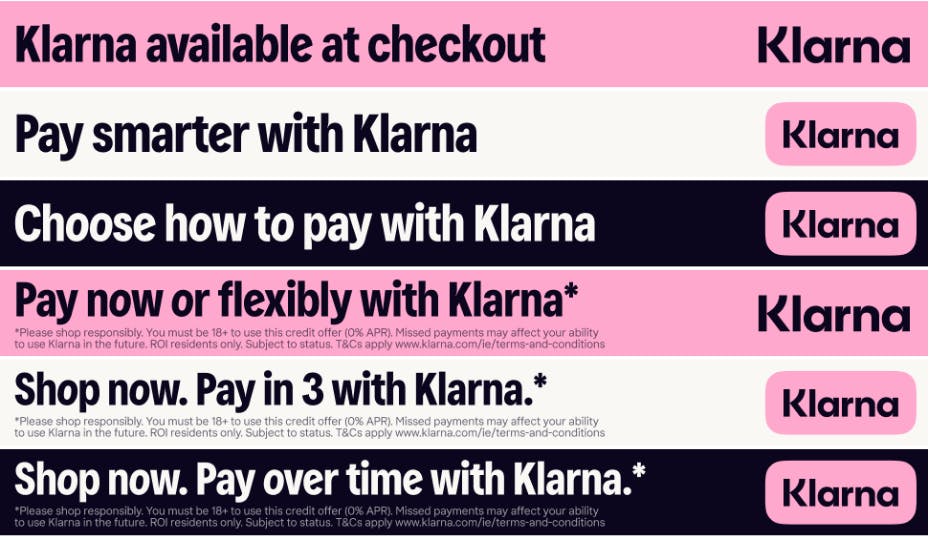

Here, you'll find a variety of Klarna-approved messaging options for your marketing touchpoints or co-marketing activities in Ireland. Download the ready-made asset packs provided below.

Downloadable ready-made assets

IE Generic banners.zip

1.1 MB

IE Pay Now banners.zip

675.5 KB

IE Pay in 3 banners.zip

1.3 MB

IE Brand kit (logo lockups).zip

120.4 KB

IE Email templates.zip

100.0 KB

Overview of the banners and logo lockups available to download

Pre-approved messaging

Generic messaging

English

Legal disclosures

Klarna available

-

Klarna available at checkout

-

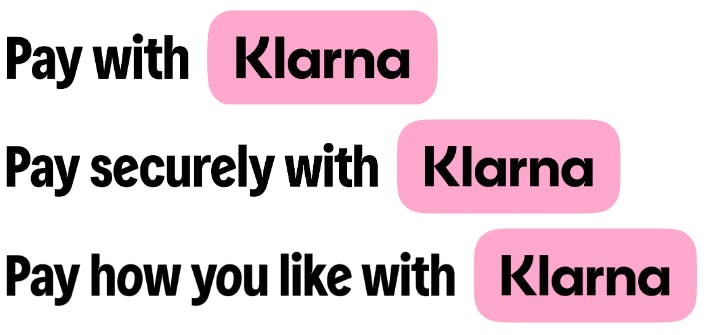

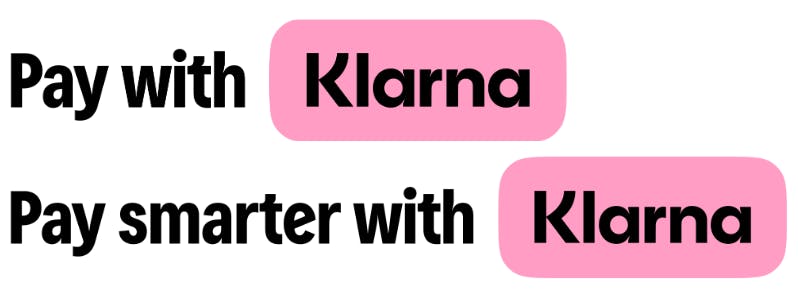

Pay smarter with Klarna.

-

Shop now. Pay with Klarna.*

*Please shop responsibly. You must be 18+ to use this credit offer (0% APR). Missed payments may affect your ability to use Klarna in the future. ROI residents only. Subject to status.

Choose how to pay with Klarna

-

Pay now messaging

English

Legal disclosures

Shop now and pay immediately.*

*Please shop responsibly. You must be 18+ to use this credit offer (0% APR). Missed payments may affect your ability to use Klarna in the future. ROI residents only. Subject to status. T&Cs apply www.klarna.com/ie/terms-and-conditions

Pay now or flexibly with Klarna.*

*Please shop responsibly. You must be 18+ to use this credit offer (0% APR). Missed payments may affect your ability to use Klarna in the future. ROI residents only. Subject to status. T&Cs apply www.klarna.com/ie/terms-and-conditions

Pay in 3 smaller payments messaging

English

Legal disclosures

Shop now. Pay in 3 with Klarna.*

*Please shop responsibly. You must be 18+ to use this credit offer (0% APR). Missed payments may affect your ability to use Klarna in the future. ROI residents only. Subject to status. T&Cs apply www.klarna.com/ie/terms-and-conditions

Split your purchases into 3 interest-free payments.*

*Please shop responsibly. You must be 18+ to use this credit offer (0% APR). Missed payments may affect your ability to use Klarna in the future. ROI residents only. Subject to status. T&Cs apply www.klarna.com/ie/terms-and-conditions

Get more time to pay with Klarna*

*Please shop responsibly. You must be 18+ to use this credit offer (0% APR). Missed payments may affect your ability to use Klarna in the future. ROI residents only. Subject to status. T&Cs apply www.klarna.com/ie/terms-and-conditions

Shop now. Pay over time with Klarna*

*Please shop responsibly. You must be 18+ to use this credit offer (0% APR). Missed payments may affect your ability to use Klarna in the future. ROI residents only. Subject to status. T&Cs apply www.klarna.com/ie/terms-and-conditions

This section only applies to:

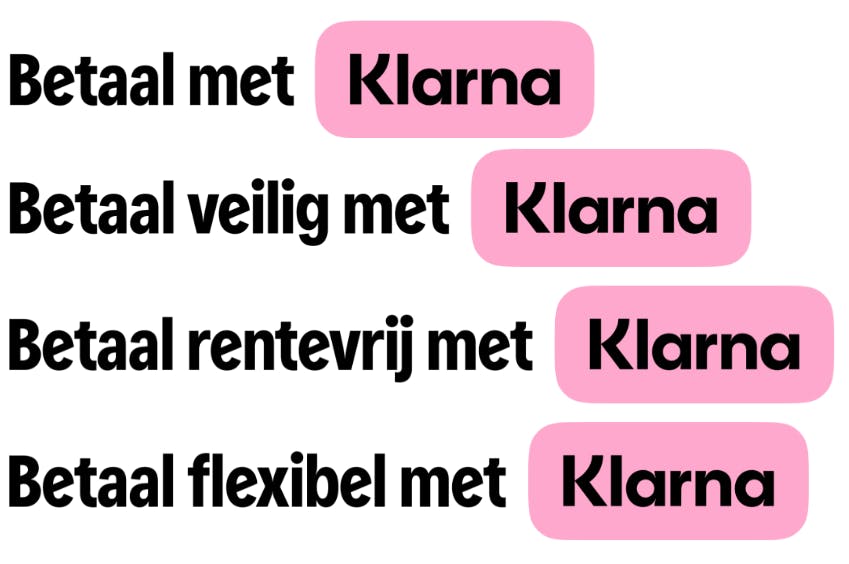

Here, you'll find a variety of Klarna-approved messaging options for your marketing touchpoints or co-marketing activities in the Netherlands. Download the ready-made asset packs provided below.

Downloadable ready-made assets

NL Generic banners.zip

855.3 KB

NL Pay Now banners.zip

396.2 KB

NL Pay Later banners.zip

965.9 KB

NL Pay in 3 banners.zip

923.8 KB

NL Brand kit (logo lock-ups).zip

490.4 KB

NL Email templates .zip

141.1 KB

Overview of the banners and logo lockups available to download

Pre-approved messaging

Generic messaging

English

Dutch

Klarna available at checkout

Klarna beschikbaar bij het afrekenen

Shop now. Pay with Klarna.

Shop nu. Betaal met Klarna.

Pay flexibly with Klarna

Flexibel betalen met Klarna

Shop now. Pay securely with Klarna.

Shop nu. Betaal veilig met Klarna.

You decide how you want to pay. With Klarna.

Bepaal zelf hoe je wil betalen. Met Klarna.

Pay now messaging

English

Dutch

Shop now and pay immediately

Shop nu en betaal direct

Pay now or flexibly. With Klarna.

Betaal nu of flexibel. Met Klarna.

Pay later in 30 days messaging

English

Dutch

Try now. Get 30 days to pay.

Probeer nu. Betaal tot en met 30 dagen later.

Shop now and pay in up to 30 days

Shop nu. Betaal tot en met 30 dagen later

Pay now or flexibly in up to 30 days

Betaal nu of flexibel tot en met 30 dagen later

Pay in 3 smaller payments messaging

English

Dutch

Shop now. Pay in 3 with Klarna.

Shop nu, betaal in 3 delen met Klarna.

Split your purchases into 3 interest-free payments

Splits je aankoop in 3 rentevrije betalingen.

Shop now. Pay in 3 interest-free payments with Klarna.

Shop nu. Betaal in 3 rentevrije betalingen met Klarna.

This section only applies to:

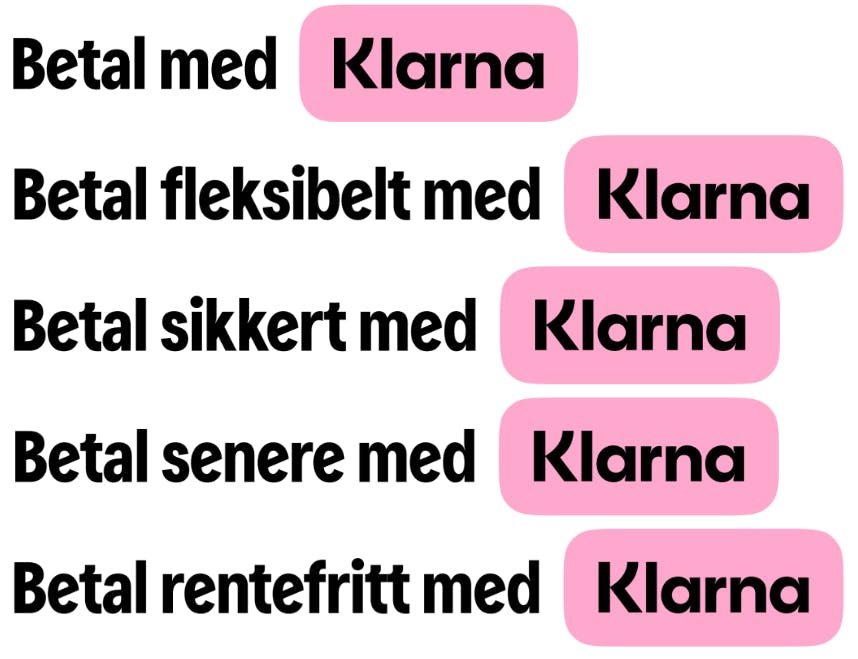

Here, you'll find a variety of Klarna-approved messaging options for your marketing touchpoints or co-marketing activities in Norway. Download the ready-made asset packs provided below.

Downloadable ready-made assets

NO Generic banners.zip

388.2 KB

NO Pay Now banners.zip

427.3 KB

NO Pay Later banners.zip

884.6 KB

NO Pay in 3 banners.zip

1.3 MB

NO Brand kit (logo lock-ups).zip

601.6 KB

NO Email templates.zip

131.5 KB

Overview of the banners and logo lockups available to download

Pre-approved messaging

Generic messaging

English

Norwegian

Klarna available at checkout

Klarna tilgjengelig i kassen

Shop now. Pay with Klarna.

Shop nå. Betal med Klarna

Pay smarter with Klarna

Betal smartere med Klarna

Pay flexibly with Klarna

Betal fleksibelt med Klarna

Pay securely with Klarna

Betal sikkert med Klarna

Pay now messaging

English

Norwegian

Shop now and pay immediately

Shop nå og betal umiddelbart

Pay now or flexibly. With Klarna.

Betal nå eller fleksibelt. Med Klarna.

Pay later in 30 days messaging

English

Norwegian

Get it. Try it. Buy it.

Få det. Prøv det. Kjøp det.

Get 30 days to pay

Få 30 dager til å betale

Shop now. Pay in 30 days with Klarna.

Shop nå. Betal om 30 dager med Klarna.

Pay in 3 smaller payments messaging

English

Norwegian

Shop now. Pay in 3 with Klarna.

Shop nå. Betal i 3 deler med Klarna.

Split your purchases into 3 interest-free payments

Del opp kjøpene dine i 3 rentefrie betalinger

Get more time to pay with Klarna

Få mer tid til å betale med Klarna

Shop now. Pay over time with Klarna.

Shop nå. Betal over tid med Klarna.

This section only applies to:

Here, you'll find a variety of Klarna-approved messaging options for your marketing touchpoints or co-marketing activities in Poland. Download the ready-made asset packs provided below.

Downloadable ready-made assets

PL Generic banners.zip

486.8 KB

PL Pay Later banners.zip

824.2 KB

PL Pay in 3 banners.zip

877.3 KB

PL Brand kit (logo lockups).zip

619.5 KB

PL Email templates.zip

140.2 KB

Overview of the banners and logo lockups available to download

Pre-approved messaging

Generic messaging

English

Polish

Legal disclosures

Klarna available

Tu zapłacisz z Klarną

-

Klarna available at checkout

Wybierz Klarnę wśród metod płatności

-

Get more time to pay with Klarna

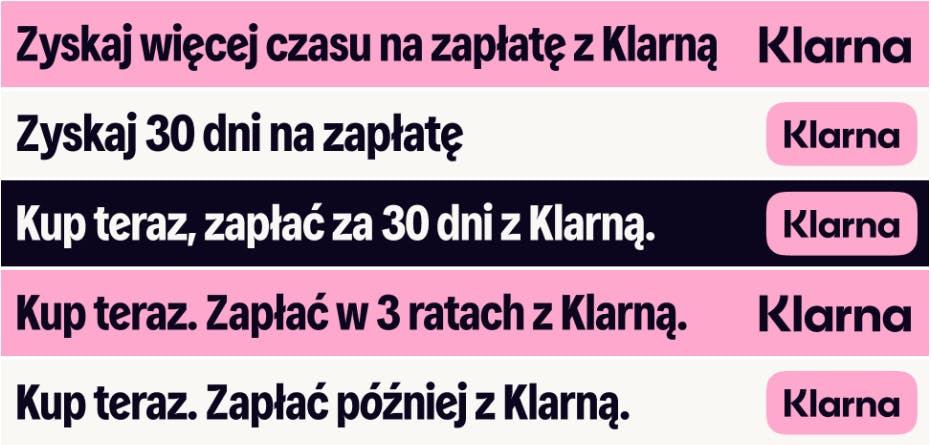

Zyskaj więcej czasu na zapłatę z Klarną

-

Pay later in 30 days messaging

English

Polish

Legal disclosures

Pay in 30 days with Klarna

Zapłać za 30 dni z Klarną

-

Get it. Try it. Buy it.

Kup. Wypróbuj. Zapłać.

-

Get 30 days to pay

Zyskaj 30 dni na zapłatę

-

Shop now, pay in 30 days with Klarna.

Kup teraz, zapłać za 30 dni z Klarną.

-

Pay in 3 smaller payments messaging

English

Polish

Legal disclosures

Pay in 3 with Klarna

Zapłać w 3 ratach z Klarną

-

Shop now. Pay in 3 with Klarna.

Kup teraz. Zapłać w 3 ratach z Klarną.

-

Shop now. Pay over time with Klarna

Kup teraz. Zapłać później z Klarną.

-

Split your purchases into 3 interest-free payments.**Delay interest will be applied in case you miss the deadline of payment

Zapłać w 3 miesięcznych ratach. Bez odsetek.*

*W przypadku opóźnień w płatności zostaną naliczone ustawowe odsetki za opóźnienie.

This section only applies to:

Here, you'll find a variety of Klarna-approved messaging options for your marketing touchpoints or co-marketing activities in Portugal. Download the ready-made asset packs provided below.

Downloadable ready-made assets

PT Generic banners.zip

1.2 MB

PT Pay Later banners.zip

508.4 KB

PT Pay in 3 banners.zip

494.7 KB

PT Brand kit (logo lockups).zip

388.7 KB

PT Email templates.zip

141.7 KB

Overview of the banners and logo lockups available to download

Pre-approved messaging

Generic messaging

English

Portuguese

Spread the cost of your purchases with Klarna

Divide o valor da tua compra com Klarna

Get more time to pay with Klarna

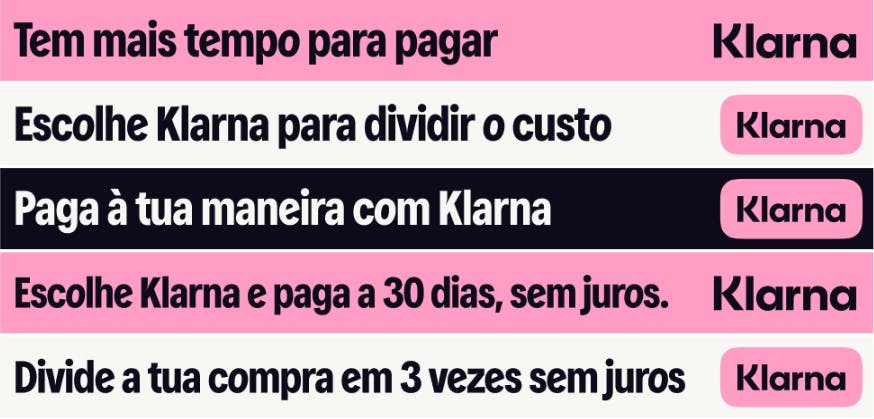

Tem mais tempo para pagar com Klarna

Choose Klarna to spread the cost

Escolhe Klarna para dividir o custo

Pay your way with Klarna

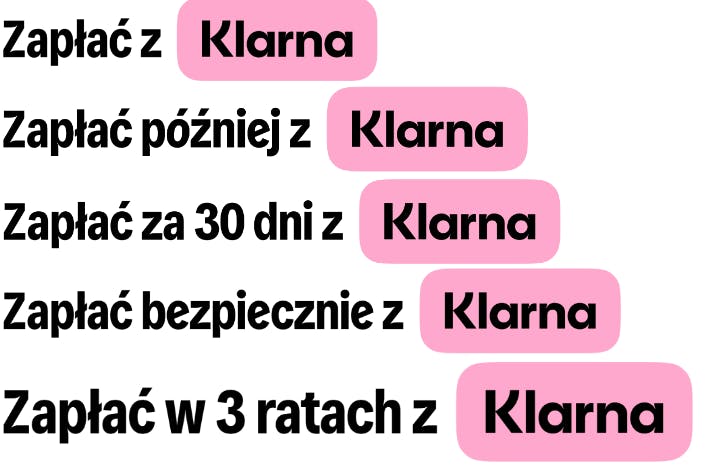

Paga à tua maneira com Klarna

Pay in 3 smaller payments messaging

English

Portuguese

Choose Klarna and pay in 3 installments

Escolhe Klarna e paga em 3 vezes sem juros.

Split your purchase in 3 payments, interest-free.

Divide a tua compra em 3 vezes sem juros

Pay later in 30 days messaging

English

Portuguese

Choose Klarna and pay in 30 days, interest-free.

Escolhe Klarna e paga a 30 dias, sem juros.

Get 30 days to pay with Klarna

Tens 30 dias para pagar com Klarna

Pay after delivery

Paga após a entrega

This section only applies to:

Here, you'll find a variety of Klarna-approved messaging options for your marketing touchpoints or co-marketing activities in Romania Download the ready-made asset packs provided below.

Downloadable ready-made assets

RO Generic banners.zip

1.2 MB

RO Pay Later banners.zip

1018.0 KB

RO Pay in 3 banners.zip

918.4 KB

RO Brand kit (logo lockups).zip

574.8 KB

RO Email templates.zip

147.9 KB

Overview of the banners and logo lockups available to download

Pre-approved messaging

Generic messaging

English

Romanian

Klarna available at checkout

Klarna este disponibilă la checkout

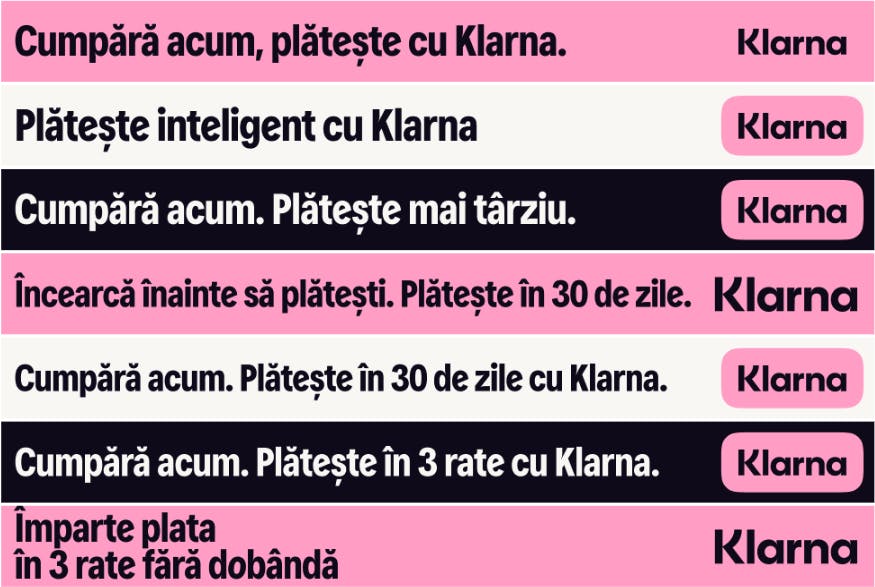

Shop now, pay with Klarna.

Klarna este disponibilă la checkout

Shop now, pay with Klarna.

Cumpără acum, plătește cu Klarna.

Pay smarter with Klarna

Plătește mai inteligent cu Klarna

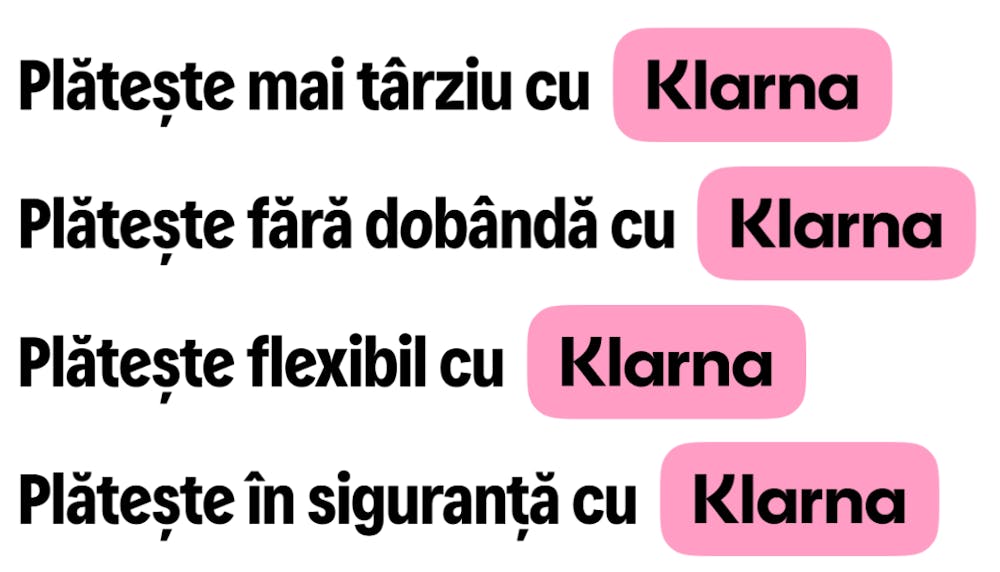

Pay flexibly with Klarna

Plătește flexibil cu Klarna

Pay securely with Klarna

Plătește siguranță cu Klarna

Shop now. Pay later with Klarna.

Cumpără acum. Plătește mai târziu cu Klarna.

Pay later in 30 days messaging

English

Romanian

Order. Try. Pay.

Comanzi. Încerci. Plătești.

Try before you pay. Pay in 30 days.

Încearcă înainte să plătești. Plătește în 30 de zile.

Shop now. Pay in 30 days with Klarna.

Cumpără acum. Plătește în 30 de zile.

Pay in 3 smaller payments messaging

English

Romanian

Shop now. Pay in 3 installments with Klarna.

Cumpără acum. Plătește în 3 rate cu Klarna.

Split your purchases into 3 interest-free payments

Împarte plata în 3 rate fără dobânda

Get more time to pay with Klarna

Obține mai mult timp pentru plată cu Klarna

This section only applies to:

Here, you'll find a variety of Klarna-approved messaging options for your marketing touchpoints or co-marketing activities in Spain. Download the ready-made asset packs provided below.

Downloadable ready-made assets

ES Generic banners.zip

1.2 MB

ES Pay Later banners.zip

431.5 KB

ES Pay in 3 banners.zip

529.0 KB

ES Brand kit (logo lock-ups).zip

682.7 KB

ES Email templates.zip

155.9 KB

Overview of the banners and logo lockups available to download

Pre-approved messaging

Generic messaging

English

Spanish

Legal disclosures

Spread the cost of your purchases with Klarna

Divide el coste de tu compra con Klarna

-

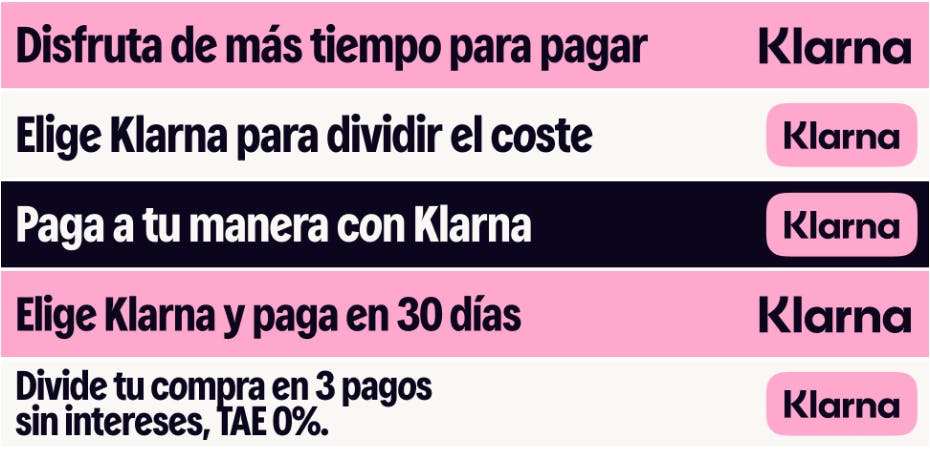

Get more time to pay with Klarna

Disfruta de más tiempo para pagar con Klarna

-

Choose Klarna to spread the cost

Elige Klarna para dividir el coste

-

Pay your way with Klarna

Paga a tu manera con Klarna

-

Pay in 3 smaller payments messaging

English

Spanish

Legal disclosures

Choose Klarna and pay in 3 installments

Elige Klarna y paga en 3 plazos

-

Split your purchase in 3 payments, APR 0%.

Divide tu compra en 3 pagos sin intereses, TAE 0%.

Included in the approved message - for more information, visit this page.

Pay later in 30 days messaging

English

Spanish

Legal disclosures

Get 30 days to pay with Klarna

Tienes 30 días para pagar con Klarna

-

Pay after delivery

Paga después de la entrega

-

Choose Klarna and pay in 30 days

Elige Klarna y paga en 30 días

-

This section only applies to:

Here, you'll find a variety of Klarna-approved messaging options for your marketing touchpoints or co-marketing activities in Sweden. Download the ready-made asset packs provided below.

Downloadable ready-made assets

SE Generic banners.zip

502.9 KB

SE Pay Now banners.zip

943.3 KB

SE Pay Later banners.zip

463.7 KB

SE Brand kit (logo lockups).zip

382.0 KB

SE Email templates.zip

142.8 KB

Overview of the banners and logo lockups available to download

Pre-approved messaging

Generic messaging

English

Swedish

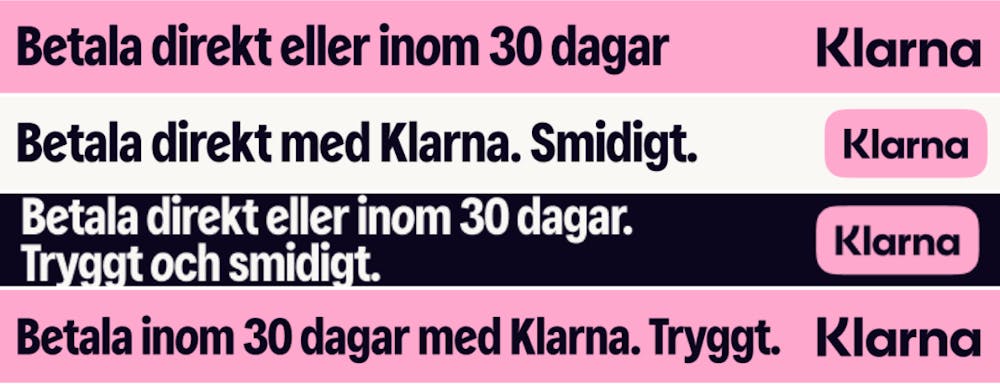

Safe and convenient

Tryggt och smidigt

Safe and convenient. Pay now or within 30 days.

Tryggt och smidigt. Betala direkt eller inom 30 dagar.

Pay now messaging

English

Swedish

Pay instantly with Klarna. Convenient.

Betala direkt med Klarna. Smidigt.

Pay instantly or within 30 days. Safe and convenient.

Betala direkt eller inom 30 dagar. Tryggt och smidigt.

Pay later in 30 days messaging

English

Swedish

Pay within 30 days with Klarna. Safe.

Betala inom 30 dagar med Klarna. Tryggt.

This section only applies to:

Here, you'll find a variety of Klarna-approved messaging options for your marketing touchpoints or co-marketing activities in Switzerland. Download the ready-made asset packs provided below.

Downloadable ready-made assets

CH (German) Generic banners.zip

408.4 KB

CH (German) Pay Now banners.zip

455.0 KB

CH (German) Pay Later banners.zip

452.6 KB

CH Brand kit (logo lockups).zip

535.9 KB

CH (German) Email templates.zip

132.0 KB

Overview of the banners and logo lockups available to download

Pre-approved messaging

Generic messaging | Generisches Messaging

English

Swiss German

Klarna available

Klarna verfügbar

Klarna available at checkout

Klarna am Checkout verfügbar

Orders, payments and returns at one glance. With Klarna.

Bestellungen, Zahlungen und Retouren auf einen Blick. Mit Klarna.

Pay flexibly and securely with Klarna

Bezahle flexibel und sicher mit Klarna

Pay now messaging | Sofort bezahlen

English

Swiss German

Pay quickly and securely. With Klarna.

Bezahle schnell und sicher. Mit Klarna.

Pay now or flexibly. With Klarna.

Bezahle sofort oder flexibel. Mit Klarna.

Pay later in 30 days messaging | In bis zu 30 Tagen bezahlen

English

Swiss German

Pay flexibly in up to 30 days.

Bezahle flexibel in bis zu 30 Tagen

Pay now or flexibly in up to 30 days

Bezahle sofort oder flexibel in bis zu 30 Tagen

Shop smart. Pay flexibly.

Shoppe smart. Bezahle flexibel.

This section only applies to:

Here, you'll find a variety of Klarna-approved messaging options for your marketing touchpoints or co-marketing activities in the UK. Download the ready-made asset packs provided below.

Downloadable ready-made assets

UK Generic banners.zip

1.2 MB

UK Brand kit (logo lock-ups).zip

121.7 KB

UK Email templates.zip

107.4 KB

Overview of the banners and logo lockups available to download

Pre-approved messaging

Generic messaging

British English

Legal disclosures

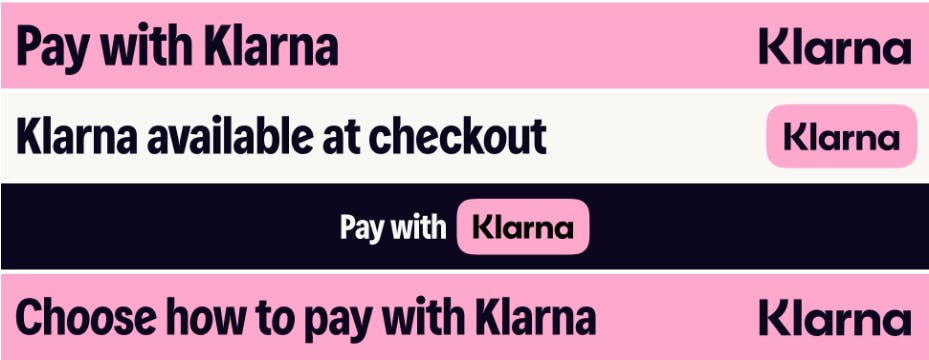

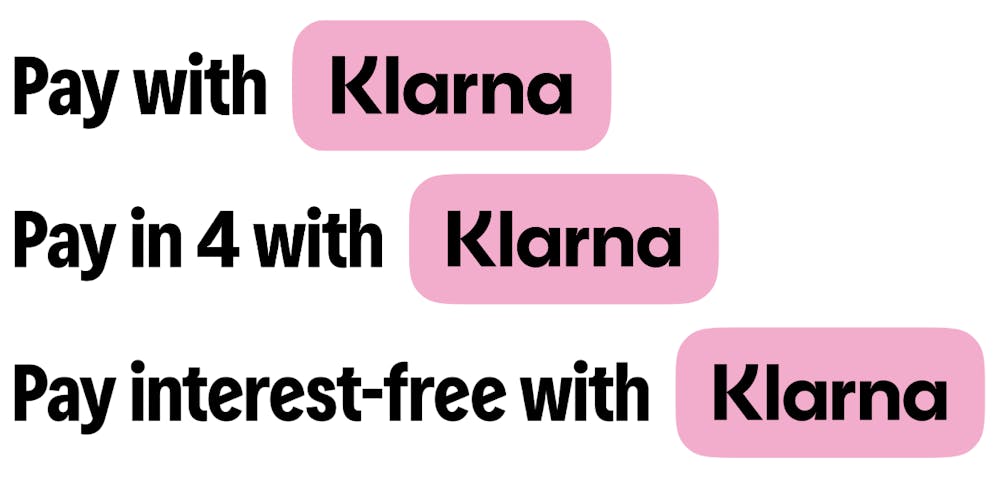

Pay with Klarna

Doesn’t trigger a disclosure. If you are amending this message, you need to follow disclosure guidance.

Klarna available

Doesn’t trigger a disclosure. If you are amending this message, you need to follow disclosure guidance.

Klarna available at checkout

Doesn’t trigger a disclosure. If you are amending this message, you need to follow disclosure guidance.

Choose how to pay with Klarna

Doesn’t trigger a disclosure. If you are amending this message, you need to follow disclosure guidance.

Here, you'll find a variety of Klarna-approved messaging options for your marketing touchpoints or co-marketing activities in Canada. Download the ready-made asset packs provided below.

Downloadable ready-made assets

CA (English) Generic banners.zip

838.2 KB

CA (English) Pay Now banners.zip

899.9 KB

CA (English) Pay in 4 banners.zip

1.1 MB

CA (English) Email templates.zip

94.2 KB

CA (French) Generic banners.zip

490.6 KB

CA (French) Pay Now banners.zip

496.9 KB

CA (French) Pay in 4 banners.zip

626.6 KB

CA (French) Email templates.zip

123.3 KB

CA Brand kit (logo lockups).zip

759.1 KB

Overview of the banners and logo lockups available to download

Pre-approved messaging

Generic messaging

Canadian English

Canadian French

Legal disclosures

Klarna available at checkout

Klarna disponible au moment de payer

Shop now, pay with Klarna.

Magasinez maintenant. Payez avec Klarna.

Shop now. Pay over time with Klarna.

Magasinez maintenant. Payez au fil du temps avec Klarna.

Pay now messaging

Canadian English

Canadian French

Legal disclosures

Shop now and pay immediately

Magasinez et payez maintenant

Pay now or flexibly. With Klarna.

Payez maintenant ou de manière flexible. Avec Klarna.

Pay in 4 smaller payments messaging

Canadian English

Canadian French

Legal disclosures

Shop now, pay in 4 with Klarna.*

Magasinez et payez en 4 versements avec Klarna.*

*See Canadian payment terms at klarna.com/ca/paylaterin4. A higher initial payment may be required for some consumers. *Voir conditions ici: www.klarna.com/fr-ca/paylaterin4/. Un paiement initial plus élevé peut être exigé pour certains utilisateurs.

Split your purchase into 4 interest-free payments.*

Do not use “interest -free” in Canadian French language or in the Province of Quebec.

*APR 0%. No conditions apply. Term: 2 months. For more information, see klarna.com/ca/legal. A higher initial payment may be required for some consumers.

This section only applies to:

MX Generic banners.zip

1.6 MB

MX Pay in 4 banners.zip

806.6 KB

MX Brand kit (logo lockups).zip

256.7 KB

MX Email templates.zip

139.1 KB

Overview of the banners and logo lockups available to download

Pre-approved messaging

Generic messaging | Mensajes genéricos

English

Mexican Spanish

Legal disclosures

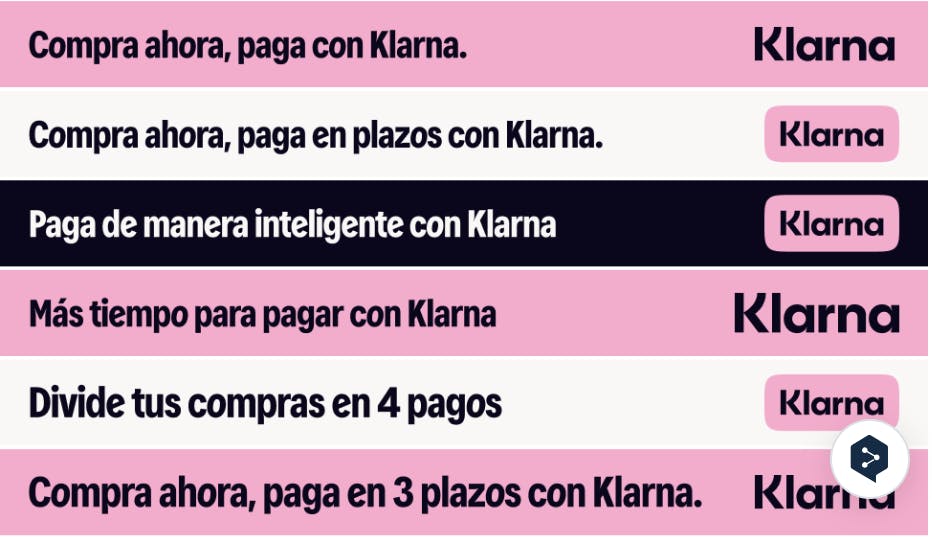

Shop now, pay over time with Klarna.

Compra ahora, paga en plazos con Klarna.

-

Shop now, pay with Klarna.

Compra ahora, paga con Klarna.

-

Pay smarter with Klarna

Paga de manera inteligente con Klarna

-

Get more time to pay with Klarna

Más tiempo para pagar con Klarna

-

Pay in 4 messaging | Mensajes de "Paga en 4 plazos"

English

Mexican Spanish

Legal disclosures

Shop now, pay in 4 with Klarna.

Compra ahora, paga en 4 plazos con Klarna.

-

Split your purchase into 4 payments

Divide tus compras en 4 pagos

-

Split your purchase into 4 interest-free payments. With Klarna.*

*APR 0%. VAT not included. For information and comparative purposes. Learn more at klarna.com.

Divide tus compras en 4 pagos sin intereses. Con Klarna.*

*CAT 0%. Sin IVA. Sujeto a aprobación de crédito. Para fines informativos y de consulta. Conoce más en https://www.klarna.com/mx/

This section only applies to:

US Generic banners.zip

1.1 MB

US Pay in 4 banners.zip

1.1 MB

US Pay Later banners.zip

789.2 KB

US Pay Now banners .zip

482.7 KB

US Financing banners.zip

500.8 KB

US Brand kit (logo lock-ups).zip

377.5 KB

US Email templates.zip

93.9 KB

Overview of the banners and logo lockups available to download

Pre-approved messaging

Generic messaging

American English

Legal disclosures

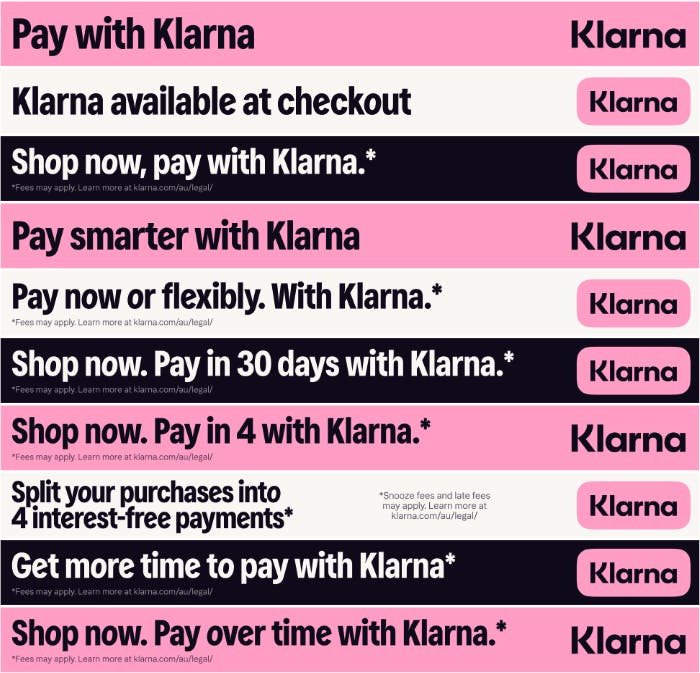

Klarna available at checkout

-

Pay smarter with Klarna

-

Find Klarna at checkout

-

Smart shoppers pick pink at checkout

-

Pick pink at checkout

-

Pay now messaging

American English

Legal disclosures

Pay now or choose how to pay with Klarna.

-

Pay now with Klarna

-

Pay later in 30 days messaging

American English

Legal disclosures

Get it. Try it. Buy it.

-

Shop now and pay later in 30 days.

-

Pay in 4 smaller payments messaging

American English

Legal disclosures

Shop now. Split your purchase into 4 interest-free payments with Klarna.*

*CA resident loans made or arranged pursuant to a California Financing Law license.

Split your purchases into 4 interest-free payments*

*CA resident loans made or arranged pursuant to a California Financing Law license.

Shop smart and split the cost into 4 interest-free payments.*

*CA resident loans made or arranged pursuant to a California Financing Law license.

Financing messaging

American English

Legal disclaimers

Pay over time with monthly financing*

*Monthly financing through Klarna issued by WebBank.

Split the cost of big purchases over 6, 12, or 36 months.*

*Rate ranges from 7.99%-33.99% APR based on creditworthiness and subject to credit approval, resulting in, for example, 12 equal monthly payments of $86.98 at 7.99% APR to $99.46 at 33.99% APR per $1000 borrowed. Minimum purchase required. A down payment may be required. Estimation of monthly payment excludes potential tax and shipping costs. Monthly financing through Klarna issued by WebBank.