Legal and data protection (EU)

Understand Klarna Payments requirements for address data protection and data sharing, use required “order with obligation to pay” button wording, and present T&Cs clearly.

When adding Klarna Payments to your site, you need to consider

- Data protection and data sharing aspects

- Required wording on order confirmation button to ensure legal obligation to pay

- T&C information

Please seek legal advice to ensure compliance with applicable regulations.

Please be aware that Klarna Payments may only be utilized at stores (both online and in-store) that have received prior approval from Klarna. Usage of Klarna Payments in any store not authorized by Klarna could result in an obligation to repay any claims arising from such unauthorized use.

Customer data sharing

National and EU rules such as the GDPR sets certain limits to how and when you may share customer identifying information with Klarna.

If you share personal data with Klarna you need to explain this in your privacy notice and link to Klarna’s privacy notice there. Below is an example of what that could look like in your existing privacy notice (the specific data categories transferred to be added, and text to be translated into your local language)

Draft privacy notice text

“In order to offer you Klarna’s payment methods, we might in the checkout pass your personal data in the form of contact and order details to Klarna, in order for Klarna to assess whether you qualify for their payment methods and to tailor those payment methods for you. Your personal data transferred is processed in line with Klarna’s own privacy notice.”

Required wording on the order confirmation button

A court ruling (case C-249-21) has established a principle regarding what copy needs to be displayed on the order confirmation button in retailers' checkout in order to legally obligate the consumer to pay. It is not enough to just state “order”; it needs to combine an order with the obligation to pay, similar to wording like “order and pay”. It is the responsibility of each individual online retailer who has integrated Klarna Payments to ensure compliance with the above-mentioned principle since the retailer controls the order confirmation button. More information can be found in KP Best Practices - payment widget.

Terms and conditions

Ensure that your terms and conditions reflect your cooperation with Klarna, and that you comply with applicable laws.

Compliance Requirements for your website

As a merchant, it is crucial to meet, among other things, the following legal requirements on your website to ensure transparency and compliance with our merchant agreement and relevant consumer protection laws (UK Consumer Rights Act 2015, German Civil Code, Swedish Law on Distance Contracts and Off-Premises Contracts).

Please ensure the information is presented clearly and understandably:

Contact Information:

- Provide your registered business address.

- List an active email address and telephone number to facilitate reliable customer contact.

Product Information:

- Ensure all product descriptions are accurate and give a true representation of the items you are selling. If you choose to include images or videos, they must also reflect a clear and honest representation of the products.

Delivery Information:

- Detail the method of delivery, estimated shipping times, and any other relevant shipping information.

Right of Withdrawal:

- Clearly outline the consumer's right to withdraw from a purchase.

- Provide a withdrawal form and specify that the withdrawal date is determined by the customer's declaration, not your response.

Return Instructions:

- Offer clear instructions on how to return a product. It’s insufficient to require customers to contact you for this information. Include the return address and any other steps, such as packaging requirements, etc, to follow.

Costs of Return:

- Clearly disclose if the consumer is responsible for the return costs in cases of withdrawal, unless the return is due to an incorrect or faulty item being sent, in which case you cover the return costs.

Use of Klarna’s Buyer's Protection:

- Do not use Klarna’s Buyer’s Protection in any promotional materials or website copy as an endorsement of the quality of your goods or your store. It is intended to reassure buyers about the purchase process, not to imply any endorsement of product quality or store reputation.

Important Notice:

Non-compliance with these requirements may significantly impact the resolution of any disputes. Adhering to the guidelines listed above is essential for maintaining trust and accountability in your dealings with customers and ensuring a favorable outcome in dispute scenarios.

This section only applies to:

Presentation considerations for Finland (FI)

Please note that you as a seller of goods and services in Finland, among others, need to adhere to the Finnish consumer protection act (Sw; Konsumentskyddslag 20.1.1978/38) chapter 6 § 12 b when integrating Klarna Payment Method in your checkout. This rule dictates how payments methods should be presented and sorted at checkout.

If you have Klarna as a single payment method on checkout, we recommend that you list the Klarna option first. If you have a need to showcase certain payment options as individual options, then you should list Pay now options first, and thereafter credit options including card payments.

This section only applies to:

Presentation considerations for Sweden (SE)

English

New consumer credit legislation - March 2025

Starting from 1 March 2025, new credit regulations will be implemented in Sweden, impacting how credit is extended and marketed. Here are the essential details you need to know:

Credit Extension Limitations: Customers opting for financing will have the opportunity to either snooze or convert their loan terms only once before the payment's due date. It's important to note that not all customers will automatically qualify for a loan conversion.

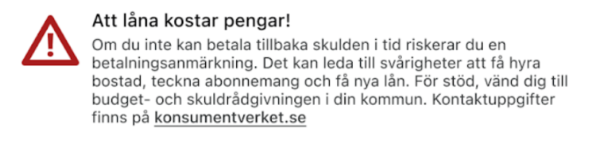

Marketing Obligations for Credit Agreements: In line with guidelines from Konsumentverket, all credit agreement promotions must include clear, upfront disclosures about the costs associated with borrowing. Advertisements must feature a bold headline stating, “Borrowing costs money!” Followed by the following risk information, “If you are unable to repay your debt on time, you risk receiving a payment default record, which can complicate future attempts to rent housing, sign subscription contracts, and secure new loans.”

Additionally, advertisements should guide customers to municipal budget and debt counseling services, with contact information accessible at konsumentverket.se.

Disclosure Requirements:

- The mandatory notice should be accompanied by a symbol, which needs to be as tall as three lines of text and appear in red.

- If the marketing message is conveyed verbally, the term “notice” should be used in place of the symbol.

- The notice should be clearly displayed in black text on a white background unless adjustments are made for digital devices set to dark mode.

Konsumenverket Example:

EN Translation:

Borrowing costs money!

If you cannot repay the debt on time, you risk a payment default. This may lead to difficulties in renting housing, signing contracts, and obtaining new loans. For support, contact budget and debt counseling in your municipality. Contact details are available at konsumentverket.se.

***

These new regulations are designed to enhance transparency in credit marketing and safeguard customers by providing them with essential information to make informed financial decisions.

New credit legislation July 2020 - How you will be impacted

New legislation has been adopted by the Swedish Parliament stating that if both credit and debit payment options are offered by a merchant, the debit option(s) must be presented before the credit option(s) in the checkout. This law takes effect 1 July 2020.

Here’s what you need to know if you have the following payment & checkout options:

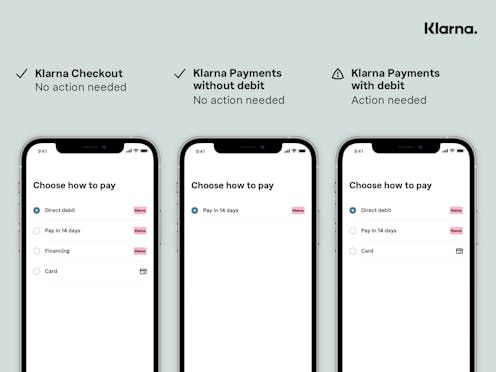

Klarna Payments (KP) with no debit options: No action required.

You are only required to make sure a debit option is placed as the first option if you offer it as a payment method.

Klarna Payment (KP) with debit options: Action required.

As a merchant, you are in control of the order in which payment methods are organized inside your checkout and will need to take steps to comply with the new law.

Continue reading for more details on how KCO will be presented, and what actions we recommend if you have KP with debit options.

What the new law means

New legislation (Regeringens proposition) adopted by the Swedish Parliament will take effect on 1 July 2020, and will only be applicable to Sweden. The law sets requirements on the presentation of payment methods in online checkouts, enforcing debit payment options to be displayed before any credit payment options, if both are available.

Obligations in the new regulation apply to any parties who present or process payment methods. This includes: merchants, partners, and Payment Service Providers (PSP) like banks. To navigate the new changes, we’ve published guidelines, to help our merchants and partners to ensure compliance with the legal requirements.

What does this mean for me as a merchant?

The impact for you as a merchant will depend on what payment methods you offer and what checkout solution you use. The new legislation does not require merchants to provide debit payment methods, but does regulate how to present them in an online checkout if you do.

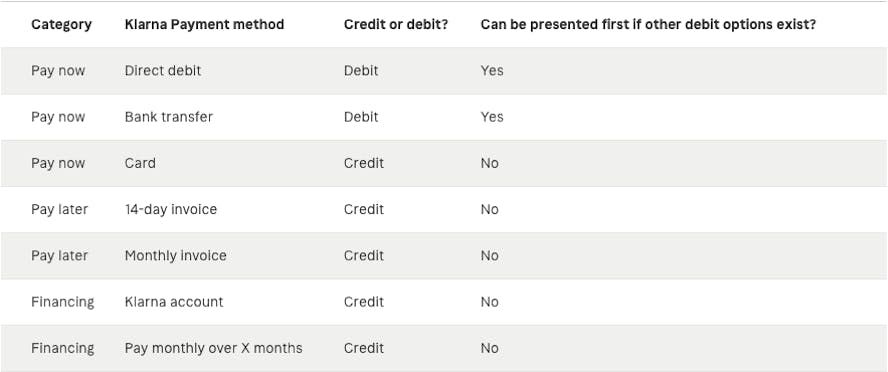

Below is an overview of Klarna payment methods, and how each categorizes in terms of credit or debit options.

What do I need to do to be prepared?

Merchants with Klarna Payments (KP)

If you offer Klarna Payments in your checkout, Klarna cannot control the order or logic in which the payment methods are presented. Therefore, as a merchant you are solely responsible to ensure your checkout is compliant and lawful according to the new legislation before it enters into force (1 July 2020).

If you have Klarna Payments (KP) and multiple Klarna payment methods within the same widget then we will manage the logic of sorting these. If a debit payment option exists then that will be displayed first. Credit payment methods that include interest rate will always be displayed as the last option if others exist. If the multiple Klarna payment methods are placed in different widgets then we cannot control in what order they will be sorted.

Klarna will discontinue support of Klarna Payment Methods (KPM) as of September 2020. Action recommended.

Klarna will no longer be supporting KPM as of September 2020. For automatic updates (including legal compliance), we recommend all merchants move to Klarna Payments (KP).

Please reach out to your Klarna account manager to get more information about pricing and how to transfer to Klarna Payments.

Swedish

Ny konsumentkreditlagstiftning – mars 2025

Från och med den 1 mars 2025 kommer nya kreditregler i Sverige, vilket påverkar hur krediter beviljas och marknadsförs. Här är de viktigaste detaljerna du behöver känna till:

Begränsningar vid kreditgivning: Kunder som väljer finansiering kommer att ha möjlighet att antingen skjuta upp eller ändra sina lånevillkor endast en gång innan betalningsförfallodagen. Det är viktigt att notera att inte alla kunder automatiskt kommer att kvalificera sig för en låneomvandling.

Marknadsföringskrav för kreditavtal: I enlighet med Konsumentverkets riktlinjer måste all marknadsföring av kreditavtal innehålla tydliga och framträdande uppgifter om kostnaderna för att låna pengar. Reklam måste ha en tydlig rubrik med texten: ”Att låna kostar pengar!” följt av följande riskinformation:

"Om du inte kan betala din skuld i tid riskerar du att få en betalningsanmärkning, vilket kan försvåra framtida möjligheter att hyra bostad, teckna abonnemang och ta nya lån."

Dessutom ska annonser hänvisa kunder till kommunal budget- och skuldrådgivning, med kontaktuppgifter tillgängliga på konsumentverket.se.

Informationskrav

- Den obligatoriska varningen ska åtföljas av en symbol, som ska vara lika hög som tre rader text och visas i röd färg.

- Om marknadsföringsbudskapet framförs muntligt ska termen "varning" användas istället för symbolen.

- Varningen ska tydligt visas med svart text på vit bakgrund, om inte justeringar görs för digitala enheter i mörkt läge.

Exempel från Konsumentverket:

Dessa nya regler är utformade för att öka transparensen inom kreditmarknadsföring och skydda kunder genom att ge dem nödvändig information för att fatta välgrundade ekonomiska beslut.

Så påverkas du av den nya kreditlagen - juli 2020

Sveriges riksdag har tidigare i år beslutat om en ny kreditlag. Den innebär i korthet att om det finns både ett kredit- och ett direktbetalningsalternativ i kassan så får inte kreditalternativet visas först eller redan vara ifyllt. Lagen träder i kraft den första juli 2020.

Här är vad du behöver veta om du har följande betalnings- och kassalternativ:

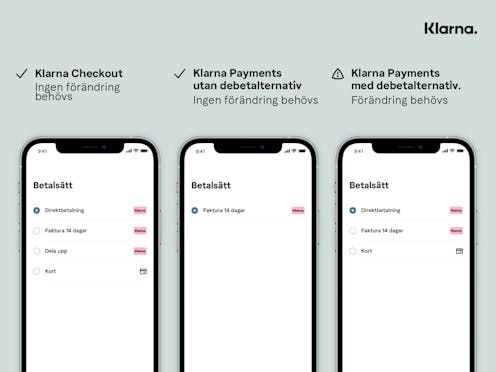

Klarna Payments (KP) utan något direktbetalningsalternativ. Du behöver inte vidta några åtgärder.

Du måste bara se till att ett direktbetalningsalternativ är det första alternativet om du erbjuder det som betalningsmetod.

Klarna Payment (KP) med ett direktbetalningsalternativ: Du måste vidta åtgärder.

Som e-handlare med Klarna Payment (KP) har du kontroll över ordningen på betalningsmetoderna som du har i din kassa och kommer därför att behöva vidta åtgärder för att följa den nya lagen.

Fortsätt läsa för mer information om hur KCO kommer att presenteras och vilka åtgärder vi rekommenderar för dig som har KP med direktbetalningsalternativ.

Vad den nya lagen innebär

Den nya kreditlagen som Sveriges riksdag har antagit (Regeringens proposition) kommer att träda i kraft den första juli 2020 och kommer endast att tillämpas i Sverige. Lagen ställer krav på hur olika betalningsmetoder presenteras i kassan, och den tvingar e-handlare att visa ett direktbetalningsalternativ före kreditalternativ, om båda alternativen finns tillgängliga i kassan.

Skyldigheterna i den nya lagen gäller alla parter som presenterar eller behandlar betalningsmetoder. Detta inkluderar: e-handlare, partners och betalningstjänstleverantörer (PSP) såsom banker. För att kunna navigera i ändringarna har vi skapat riktlinjer för att hjälpa våra e-handlare och partners att anpassa sig så att de nya lagliga kraven uppfylls.

Vad innebär det här för mig som handlare?

Exakt hur du påverkas beror på vilka betalningsmetoder som du erbjuder och vilken kassalösning som du har valt. Den nya lagen kräver inte att en handlare måste erbjuda ett direktbetalningsalternativ, utan styr hur betalningsalternativen presenteras i kassan.

Nedan finns en översikt över Klarna betalningsmetoder, och hur de kategoriseras i termer av kredit- eller direktbetalningsalternativ.

Vad behöver jag förbereda?

Handlare med Klarna Payments (KP)

Om ni erbjuder Klarna Payments i er kassa så kan inte Klarna kontrollera i vilken ordning betalningsalterntiven presenteras. Det innebär att det är den enskilda handlaren som är ensam ansvarig för att se till att er kassa är kompatibel och följer den nya lagstiftningen innan den träder i kraft (1 juli 2020).

Om ni har Klarna Payments (KP) och flertalet betalningsmetoder via Klarna inom samma modul så kommer Klarna att sortera dessa. Om det finns ett direktbetalningsalternativ så kommer det att presenteras först. Kreditalternativ som inkluderar ränta kommer alltid att att presenteras sist om det finns andra val tillgängliga. Om flera betalningssätt med Klarna är placerade i olika moduler kan Klarna ej kontrollera i vilken ordning de presenteras.

Klarna kommer att sluta stödja Klarna betalningsmetoder (KPM) från och med september 2020. Åtgärd rekommenderas.

Klarna kommer inte längre att stödja KPM från och med september 2020. För att få automatiska uppdateringar (inklusive juridisk efterlevnad) rekommenderar vi att alla handlare migrerar till Klarna Payments (KP). Prata gärna med din kontakt på Klarna för att få mer information om priser och hur du flyttar över till Klarna Payments.