Financial services are highly regulated. This means that Klarna and our merchants who advertise with us need to follow the laws and regulations that govern advertising financial products.

The following Financing Advertising Guidelines provide a general overview of the requirements you need to follow when advertising Klarna’s financing products offered in partnership with WebBank. Remember that it is also your responsibility to learn and understand the laws governing the advertising of financial products.

If you ever have any questions, please reach out to your Klarna marketing contact or us.comarketing.support@klarna.com.

This Financing Advertising Guideline should be reviewed along with the Pay in 4/Pay in 30 Advertising Guideline, along with the Legal Disclosure Table and the Social Media Disclosures

If your ad mentions monthly financing, the following disclosure is required to be included in the marketing materials.

- Disclosure: *Monthly financing through Klarna issued by WebBank.

Examples of messaging that references monthly financing (this list is not exhaustive).

- Pay over time with monthly financing.*

If your ad mentions both Pay in 4 and/or Pay in 30 and monthly financing, the following disclosure is required to be included in the marketing materials:

- Disclosure: *Monthly financing through Klarna issued by WebBank. Other CA resident loans made or arranged pursuant to a California Financing Law license.

If you list payment terms when referring to Klarna’s monthly financing products offered through Klarna’s partnership with WebBank, you need to understand the Truth-in-Lending Act. Please review the next sections carefully.

You have to disclose important terms of credit to a consumer when you advertise Klarna’s financing products offered in partnership with WebBank. When advertising terms of this type of credit, advertisements can only state terms that are actually available. When you mention specific terms of credit (called “trigger terms”), TILA requires you to provide the full terms of repayment. The best way to do this is by using a representative example of what a real loan might look like. This helps consumers understand what they are agreeing to.

The following are examples of trigger terms. If you use these, you need to provide a representative example.

- The periodic payment amount (e.g., $60/every month).

- The number of payments or period of repayment (e.g., 6 payments or 6 months).

- The amount of interest.

- The amount or percentage of any down payment.

The following words aren’t trigger terms. If you use them without the above mentioned trigger terms, you don’t need to include a representative example.

- Klarna.

- Monthly payments.

- Pay later.

- Pay in 4.

- Pay in 30 days.

If you use a trigger term, you have to provide a representative example. A representative example shows what a typical loan looks like and needs to include the following information:

- Purchase price.

- Monthly payment amount (see below for more information)

- Length of loan term.

- Annual percentage rate (APR) (see below more information)

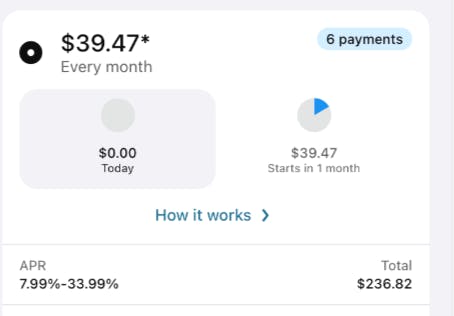

Closed (term loan) representative example

For the closed term loan financing product, you need to include the following in the representative example, which can be provided in graphic form:

- Monthly payment.

- Number of months.

- Total payment.

- Amount of any down payment.

- Annual percentage rate (please note that the APR in a representative example should always be (i) the rate available to the majority of consumers or (ii) the median rate).

Closed (term loan) disclosure

You must also include the following legal disclosure below the graphic:

*Estimated amount based on 19.99% APR. Down payment may be required. Klarna Monthly Financing issued by WebBank. Klarna and WebBank may do a soft credit check to assess eligibility. This will not impact your credit score. See terms.

This needs to be updated manually each time this is placed in an advertisement or on a merchant website. Please see below for more information.

If you have any questions or are unsure, please reach out to your Klarna representative for advice.

The best way: put the representative example [on the same creative] as the trigger term—in close proximity, and in a similar font size.

Alternative: If there simply is no space to fit the representative example on the content/creative, you have to link to a landing page (educational page about Klarna) where the representative example is clearly and conspicuously displayed. The representative example needs to be within one click of the trigger term.

You should always have a Klarna educational page on your site. This page will educate your customers about Klarna’s products and make required disclaimers and disclosures. Your Klarna educational page can be automatically generated using Klarna’s On-Site Messaging tools, using these guidelines.

Emails

Emails with TILA trigger terms must include the full terms of repayment or a representative example in the email itself, not one click away. Please ensure that you have reviewed this Financing section and the legal disclosures table to ensure all appropriate disclosures are included.

- If the subject line has a trigger term, a representative example needs to be clear and conspicuous in the body of the email.

- The subject line and sender must be accurate and not misleading.

- If the body of the email has a trigger term, a representative example needs to be clear and conspicuous and near the trigger term.

- Marketing emails must include an opt-out mechanism, and cannot be sent to customers who have opted out of marketing emails.

- Marketing emails must comply with the CAN-SPAM requirements.

If your ads are in a Video and/or TV-spot

For any videos/TV spots that mention trigger terms, a representative example needs to be included.

- All other relevant legal disclosures must be made.

- Disclosures can be verbal or shown on screen.

- Disclosures must be legible to a reasonable person (8 pt. or larger).

- Introduction of disclosures: Be sure they’re introduced at the same time as or before the trigger term, with enough video left to keep it on screen for the required length of time.

- Disclosures can be over any visual as long as they’re visible at the bottom.

- Disclosures need to be based on a reading time of 3 words/second.

If you advertise using phone calls or text messages, then you are subject to the Telephone Consumer Protection Act (TCPA) and the requirements of carriers. These laws and rules require prior express written consent to send advertising via (a) calls to traditional home, business, or wireless phones or (b) texts to wireless numbers, among numerous other requirements. For example, you may not contact anyone on the national do not call registry.

The TCPA and carrier requirements are complex, and violating them comes with the potential for lawsuits and fines. You should obtain the advice of your own lawyers before sending advertising via telephone or text.

Do not use the following terms:

- “No fees” or similar

- “No credit checks/Application”

- “Free” or similar

- If coupons/discounts/rewards are offered, they should be redeemable across all tender types, including Klarna.

- Avoid “no money down” deferral messages when advertising Klarna as a financing option. Depending on eligibility criteria, certain customers may be asked to make a down payment at checkout.

If you are ever in doubt, contact us.comarketing.support@klarna.com.

In addition to what we have covered so far, your advertising must also follow all of the laws that apply to financial advertising and advertising generally. This section summarizes key laws and regulations.

Unfair, deceptive, or abusive acts and practices can cause significant financial injury to consumers, erode consumer confidence, and undermine the financial marketplace. UDAAP was established to prevent consumer harm by misleading or deceitful actions. There are both federal and state UDAAP laws and regulations.

What you need to do.

- Include all relevant information.

- Be clear.

- Be easy to understand.

- Don’t create a false sense of urgency (e.g., Act Now!)

- Don’t encourage debt.

- Be honest.

What else you need to know.

- Disclosures don’t eliminate UDAAP risk - disclosures provide additional context. They do not negate misrepresentations, omissions, or other deceptive statements.

- Substantiate your claims - you have to have a factual basis underlying statements about any product.

- You have to honor promotions & rebates - all promotions offered must be honored, including any “risk free” trials, 0% APR financing, or money back guarantees.

- It doesn’t matter if you meant well - your intent does not matter. If you make a deceptive statement or cause harm to consumers, you committed an unfair or deceptive act.

Fair lending applies to the entire lifecycle of a loan, including advertisement of the credit product. The Equal Credit Opportunity Act (ECOA) is a law that requires credit products, like those offered by Klarna, to be advertised fairly to everyone.

- Avoid discouraging individuals from applying.

- Retailers cannot impose additional application requirements to the Klarna application process.

- Target a broad demographic.

- While a retailer may be inherently attractive to a particular demographic, the retailer should avoid targeting Klarna financing on a prohibited basis. Prohibited bases include race, color, religion, national origin sex/gender identity, marital status, age (provided the applicant has the capacity to contract), and income dependency on a public assistance program.

The CAN-SPAM Act covers all commercial messages, which the law defines as “any electronic mail message the primary purpose of which is the commercial advertisement or promotion of a commercial product or service,” including email that promotes content on commercial websites. CAN-SPAM includes business-to-business email. The Federal Trade Commission has provided the below guidance to comply with CAN-SPAM:

- Don’t use false or misleading header information. Your “From,” “To,” “Reply to,” and routing information—including the originating domain name and email address—must be accurate and identify the person or business who initiated the message.

- Don’t use deceptive subject lines. The subject line must accurately reflect the content of the message.

- Identify the message as an ad. You must disclose clearly and conspicuously that your message is an advertisement.

- Tell recipients where you’re located. Your message must include your valid physical postal address. This can be your current street address, a post office box you’ve registered with the U.S. Postal Service, or a private mailbox you’ve registered with a commercial mail receiving agency established under Postal Service regulations.

- Tell recipients how to opt out of receiving future email from you. Your message must include a clear and conspicuous explanation of how the recipient can opt out of getting email from you in the future. Craft the notice in a way that’s easy for an ordinary person to recognize, read, and understand. Creative use of type size, color, and location can improve clarity. Give a return email address or another easy internet-based way to allow people to communicate their choice to you. You may create a menu to allow a recipient to opt out of certain types of messages, but you must include the option to stop all commercial messages from you. Make sure your spam filter doesn’t block these opt-out requests.

- Honor opt-out requests promptly. Any opt-out mechanism you offer must be able to process opt-out requests for at least 30 days after you send your message. You must honor a recipient’s opt-out request within 10 business days. You can’t charge a fee, require the recipient to give you any personally identifying information beyond an email address, or make the recipient take any step other than sending a reply email or visiting a single page on an Internet website as a condition for honoring an opt-out request. Once people have told you they don’t want to receive more messages from you, you can’t sell or transfer their email addresses, even in the form of a mailing list. The only exception is that you may transfer the addresses to a company you’ve hired to help you comply with the CAN-SPAM Act.

- Monitor what others are doing on your behalf. The law makes clear that even if you hire another company to handle your email marketing, you can’t contract away your legal responsibility to comply with the law. Both the company whose product is promoted in the message and the company that actually sends the message may be held legally responsible.